A Look Into My Leadership Journey with Femeconomy

Whiteark is a proud member of Femeconomy, an organisation that supports and empowers female leaders and entrepreneurs.

I am delighted to have the opportunity to share my leadership experience with Femeconomy's audience and to our followers too.

Whiteark is a proud member of Femeconomy, an organisation that supports and empowers female leaders and entrepreneurs.

I am delighted to have the opportunity to share my leadership experience with Femeconomy's audience and to our followers too.

MY EXPERIENCE

Being a CFO at Whiteark, I have had the opportunity to lead our company through a period of immense change.

I have been able to work with small and medium enterprises in order to help them achieve their goals.

WHAT IS OUR APPROACH?

Our approach is hands-on. We work with the Board, CEO, and Leadership team to understand the problem/opportunity and what is required to delivered on this.

Our commercial experienced team is handpicked to ensure we help the organisation deliver on the outcomes.

MY BELIEFS

As a proud entrepreneur, I strongly support Femeconomy's mission to inspire and empower women in the workplace.

I believe that providing Femeconomy's readers with insights on my career trajectory will allow them to identify components of their own professional journey that can be applied to any female-dominated industry.

Check this interview HERE as I share my leadership journey as a CFO and Founder.

Disclaimer: This interview was first published by Femeconomy

Source: https://femeconomy.com/jo-hands-founder-director-whiteark/

Article by Jo Hands, Whiteark Founder

Read more articles written by Jo Hands

Need help devising a strategy? Reach out.

Working closely with boards and senior leadership, we provide a blend of strategy, market insights, and operational expertise to drive results for clients. We understand that no two businesses are the same and will tailor our advice to meet your specific needs.

If you need advice on where to start reach out to Jo Hands or an expert from our team on whiteark@whiteark.com.au

What does 2022 hold?

When the clocks strike midnight on the 31st December 2021, I’m going to be ready to yell Happy New Year bring on 2022. While 2021 has been a good year, there is a lot of look forward to for 2022.

When the clocks strike midnight on the 31st December 2021, I’m going to be ready to yell Happy New Year bring on 2022. While 2021 has been a good year, there is a lot of look forward to for 2022.

My key 3 focus areas for 2022 are:

Reflections for 2021

WOW 2021 started with some much excitement that we have got through 2020 and it was a new beginning, but it wasn’t quite what we all expected. I’m not complaining, and I have nothing to complain about, but it has definitely given me more perspective. There have been times in 2021 with the pandemic, lock downs, earthquake, floods, wind, no power that I thought the world was going to end, but here we all are still.

WOW 2021 started with some much excitement that we have got through 2020 and it was a new beginning, but it wasn’t quite what we all expected. I’m not complaining, and I have nothing to complain about, but it has definitely given me more perspective.

There have been times in 2021 with the pandemic, lock downs, earthquake, floods, wind, no power that I thought the world was going to end, but here we all are still.

I have 4 main reflections from 2021:

Are you clear on what you want to achieve?

Goals are part of every aspect of business and life. They provide a sense of direction, motivation, focus, and clarify importance. By setting goals, you are providing yourself with a target to aim for - without a goal, your efforts can become disjointed and often confusing.

Goals are part of every aspect of business and life. They provide a sense of direction, motivation, focus, and clarify importance. By setting goals, you are providing yourself with a target to aim for - without a goal, your efforts can become disjointed and often confusing. Goals will influence how and where energy and resources are used. Goals provide a destination for you to get to, so they encourage motivation and reduce procrastination. By setting goals you can measure your progress. Once you reach your goal, it gives you a taste of victory and you will want to taste that again so you will set yourself new goals.

Effective hybrid working starts with company culture

Colin D Ellis, an award-winning speaker, facilitator, and best-selling author has recently released his new book – ‘The Hybrid Handbook’. Colin covers the 6 Considerations your organisation needs to address to implement a successful Hybrid Working Model.

Colin D Ellis, an award-winning speaker, facilitator, and best-selling author has recently released his new book – ‘The Hybrid Handbook’. Colin covers the 6 Considerations your organisation needs to address to implement a successful Hybrid Working Model.

To secure your talent pool for future success, you need to move quickly on implementing your Hybrid Working Model to be considered an employer of choice. It’s time to start working through your checklist.

Do you have all the elements for a strong company culture?

Company culture can be defined as a set of shared values, goals, attitudes and practices that characterise a company. Company culture impacts all facets of the business, from recruitment to retention to performance. Organisations with strong corporate cultures have been linked to higher retention rates and increased engagement.

Company culture can be defined as a set of shared values, goals, attitudes and practices that characterise a company. Company culture impacts all facets of the business, from recruitment to retention to performance. Organisations with strong corporate cultures have been linked to higher retention rates and increased engagement.

Company culture is a naturally occurring phenomenon; your company will develop a culture whether intentional or not. Culture is influenced by a company’s mission statement, core values, beliefs and attitudes, appetite and success of innovation, work environment, employee benefits, charitable and social events and flexibility/business working hours.

Post Covid-19 culture is going to play an extremely important role in retaining and attracting top talent. Has your organisation considered what changes need to be made to create/maintain a strong company culture post covid-19?

How to find new customers during COVID

During yet another lockdown it’s hard to reach out and acquire new customers. You are busy managing your family, your own mental health, plus you actively try to keep morale high at work too. To reach new customers, you will want to understand how they have changed. How did their shopping preferences, their daily routines, their work lives change? Let’s explore these questions together.

During yet another lockdown it’s hard to reach out and acquire new customers. You are busy managing your family, your own mental health, plus you actively try to keep morale high at work too. To reach new customers, you will want to understand how they have changed. How did their shopping preferences, their daily routines, their work lives change? Let’s explore these questions together.

Developing your lead generation strategy

Since the onset of COVID-19, businesses have had to find new and clever ways to connect with their customers to generate sales and maintain relationships – this has led to the acceleration of digitisation as more customers shifted to online.

Since the onset of COVID-19, businesses have had to find new and clever ways to connect with their customers to generate sales and maintain relationships – this has led to the acceleration of digitisation as more customers shifted to online.

Customers now have the power to dictate when and where companies can interact with them. Organisations that are customer experience-minded and leverage communication technology to engage with today’s customer in the way they prefer – in the right channel, at the right moment, with the right information, will be most successful in converting leads.

Have you analysed the change in your customers’ behaviours to help better manage them and improve your customer experience?

The question on everyone’s mind - how will customers behave post the pandemic?

The question on everyone’s mind - how will customers behave post the pandemic?

A pandemic is temporary but it will influence temporary behaviours into fundamental shifts - some things will revert to pre-covid, some things will look very different, and other things will be gone for good. Covid-19 propelled a whole new generation of digital adopters online with about 70% planning to keep using the new channels permanently. It is critical for companies to improve their online offerings to provide a competitive experience for digital adopters. The quality of the customer experience remains an influential buying factor. To improve the customer experience overall, organisations need to understand the changing wants, needs and expectations of their target customer in terms of product/service offerings, the channels they use to interact/engage and when they use these channels.

There is no one size fits all option

When redesigning your company’s ways of working it’s critical that you design a model that intentionally and thoughtfully supports your business operations.

The covid-19 pandemic has fuelled the remote working trend that was already underway – it has accelerated the shift toward more flexible and customised models. If companies don’t reinvent their people strategy and how they support their employees, they will lose in the new reality. This week’s focus will be on “Ways of Working and Your People Strategy”.

Business leaders have the opportunity and imperative to redesign the future of work to unleash a new wave of human creativity and productivity. The new design will need to have intent and requires effort, leadership engagement and innovative thinking. This will result in unlocking new talent, creativity, and productivity benefits.

When redesigning your company’s ways of working, it is fundamental that you adopt a broad and holistic approach while considering the value at risk to revenues, efficiencies, customer and employee satisfaction, retention, acquiring new talent, sustainability, and wellness.

The key questions to ask - why? what? how?

Are you one of those people that asks a lot of questions – why are we doing this? What is this all about? And How are we going to deliver this? Simple words and questions but critical in all aspects of business. I have to admit it does annoy me when people ask too many questions, but it really is good engagement. It means they are engaged, they are listening and they want to understand the background.

Are you one of those people that asks a lot of questions – why are we doing this? What is this all about? And How are we going to deliver this? Simple words and questions but critical in all aspects of business. I have to admit it does annoy me when people ask too many questions, but it really is good engagement. It means they are engaged, they are listening and they want to understand the background.

Sometimes our communication gets so bogged down that it’s hard to follow – and it’s hard for people to come on the journey because they don’t understand the basics. As a leader being able to article the Why, What and How of a companies:

Strategy

Overall Plan

Particular Change

Is critical.

Right now as we run into the new financial year (for most companies) this comes more important. It’s a great opportunity to use these questions to speak to your team about the new financial year. To think about how to frame things up and get people onboard.

Why?

Definition of Why:

The cause, reason, or purpose for which know why you did it that is why you did it.

The power of the Why.

Employees are more focused than ever on the Why. Fundamentally why does this company exist? They are looking for value, purpose in why the company exists. Some companies have this and other companies this becomes a challenge. Do you understand your why? Does it resonate with the employees? Is it truthful and focused? Have you communicated it. It’s important that as a leader you understand the why and can articulate this to the team.

Simon Sinek famously talks about Starting with the Why in his famous books and ted talks.

Start With Why shows that the leaders who’ve had the greatest influence in the world all think, act, and communicate the same way — and it’s the opposite of what everyone else does. Sinek calls this powerful idea The Golden Circle, and it provides a framework upon which organizations can be built, movements can be led, and people can be inspired. And it all starts with WHY.

Why?

Definition of Why:

Asking for information specifying something.

The cause, reason, or purpose for which know why you did it that is why you did it.What are we going to deliver this year? What are the initiatives, what are the funding and plan of what we will deliver over the next 12 months. Being clear on the plan and how it links to the Why. Making sure what we are doing is linked with the Why is critical. If the What is not aligned to the Why it becomes meaningless.

Research has shown that companies that have more than 5 priorities deliver less than 18% of their plans. Being clear on your priorities and the alignment to the Why is critical. There is no point having a Why and What if you can’t deliver the how.

How?

Definition of How:

In what way or manner; by what means.

Maybe this is the most important question and people miss this step. If you have a clear why and what – how are you going to deliver? How are you going to operate (values, operating rhythm), what is the plan to get you there? How are linking strategy to execution to ensure the why and what build a plan on the how. The how is normally missed and means that you are not delivering the outcomes you want to achieve.

Most companies are focused on providing a ‘why’ for their teams. Finding that ‘purpose’, that reason to associate with the brand that is not about filling pockets of shareholders. This is a hard one. More and more there is a challenge for employers to represent meaning in working for their company. Employees are demanding this and Employers and trying to align the Why story…but it’s a struggle.

The ability to be able to communicate the

Why

What

How

consistently, effectively and in an aligned manner is critical.

Key things to think about when communicating with your employees:

Being able to articulate the Why of your company?

Being able to articulate the What – are you trying to achieve?

Being able to articulate the How – are you going to do this?

Keeping communication simple and consistent is critical. Take the time to ensure you understand and you articulate this to your employees.

Life's a journey - what does this mean?

One piece of advice my dad gave me, was to remember that life is a journey. It’s hard when you are 20 years old to really know what this means?

As I get older, a ripe old age of 42 I really consider this concept of journey. It’s an interesting one, very personal and something that evolves.

One piece of advice my dad gave me, was to remember that life is a journey. It’s hard when you are 20 years old to really know what this means?

As I get older, a ripe old age of 42 I really consider this concept of journey. It’s an interesting one, very personal and something that evolves.

The dictionary says that journey is – an act of travelling from one place to another. Where are we travelling too? What is this journey of life. Wow, very deep thing to think through.

I am not sure I have the degree to make an assessment on where we are heading, I can definitely focus on what this journey needs to look like, what is a successful journey.

In business, when we start a program we normally start by designing the end-state view – what does success look like, where are we heading and what are the key design principles that need to be determined in relation to this. This sets the course, direction and gives people something to anchor too. It makes decisions easier and allows people to work towards a common goal. I suppose life is not that simple – what is the end state you are building and what are the design principles to make decisions around your journey? Maybe that is why people talk about what you want people to say at your funeral, that is quite depressing but maybe they are trying to design this end state view to build the guardrails for the journey. On the journey of life it’s probably not that easy.

To define success for your journey, you should consider the following:

What makes you happy – do more

What are you good at – do more

What is aligned to your strengths – do more

What develops you / stretches you, in the right direction – do more

What allows you to associate with people that inspire and challenge you – do more

What makes you miserable – do less

What makes you uninspired – do less

What makes you focus on counting down the week – do less

You know in your gut it’s not good for you – do less

So many more rules you could apply, but you get the drift. You need to determine what you are going to do in your journey, it’s like a choose your own adventure book… you remember you can pick which direction you took the characters on. The reality is life, is like a choose your own adventure, but there are also things that you can’t control that will land in your lap and how you respond.

When thinking about the journey, people reference sprint versus marathon and ensuring you don’t go to quick you burn yourself out and you enjoy the journey. Everyone has a different pace, but sometimes you do need to slow down – for your health, for your family, to slow down to speed up, so people can keep up.

What is your pace?

Enjoying the journey, as you get older you realise that you need to enjoy the journey – life’s short. Time speeds up and making the best of every time you have in life is so critical. This means spending time with people that inspire, challenge and encourage you. Caring about their opinions but not listening to others. Embracing yourself, imperfections and all and do what makes you happy.

On the journey there will be great days, there will be speed humps and there will be an accident on the freeway that will stop you in your tracks. The hardest days are the ones that will demonstrate to yourself your tenacity, your passion and your ability to keep going. While you are in the moment, it will appear too much and once your through you will proud of your achievement.

Remember take time on the journey for a breather – to reflect what you have achieved, where you are and how you are going to continue on your journey. You continue to learn lessons, some the hard way that may change your journey, how you approach your journey or your destination.

Regardless of what you see on social media, no one has a perfect life. So be kind to yourself, to others and don’t compare, just enjoy your journey and make sure you have some great people on the way you can share the journey with!

I know that on my journey I want to make a difference to people’s life for the better. I am passionate about helping businesses optimise and I hope that I can leave a legacy in working with businesses to drive success.

How to Master Delivery

The plan is built, you have the budget, why can’t you deliver?

It’s the issue that is widely known, the easy part is building the plan and getting the money (well sometimes) but being able to deliver the plan is the hard thing. When the plan is unclear or money hard to get it’s a good excuse, when that’s done there are no excuses you need to be able to Execute.

At Whiteark this is where we see our clients need help and this is our sweet spot, being able to help deliver a program of work. There are 4 key steps that need to be taken to ensure the plan is successfully executed.

The plan is built, you have the budget, why can’t you deliver?

It’s the issue that is widely known, the easy part is building the plan and getting the money (well sometimes) but being able to deliver the plan is the hard thing. When the plan is unclear or money hard to get it’s a good excuse, when that’s done there are no excuses you need to be able to Execute.

At Whiteark this is where we see our clients need help and this is our sweet spot, being able to help deliver a program of work. There are 4 key steps that need to be taken to ensure the plan is successfully executed.

Key four steps:

Step 1: A detailed plan is required.

The plan must be very detailed and provide information on the following:

Tasks

Timeframe

Responsible Party

How success will be measured

Building out the program is critical with the required detail to measure if things are offtrack and the flow on impacts. Understanding key dependencies is critical and managing them as well (in this case Technology Services).

Step 2: The right capability must be identified to execute the plan

This might be a mix of internal capability, partners and other consultants but being clear on roles & responsibilities and having the right capability to:

Deliver the required outcome

Do it at a speed that is sustainable

Deliver the right outcome

Allow coaching and training so the team left behind after the project are upskilled and can do it without external help

Step 3: Flexibility to pivot, change direction & work some of the program out along the way is critical.

The original plan won’t work perfectly, the program needs to allow an element of flexibility when things don’t go to plan, you identify something else along the way.

Step 4: Sponsorship.

Strong sponsorship on the program. Executive sponsorship that is willing to go into battle will be critical. Absolutely critical. There will be roadblocks, issues that prevent the program moving and you need someone to move these out of the way and be focused on seeing the program deliver.

What we know from experience is?

All four steps are required to ensure effective execution. Things don’t always go to plan, but having a clear plan to be able to pivot or make changes in the program is critical.

But just start, the team will see change, will embrace the change and lean it but just start the program, piece of work and get delivering. It will give you credibility, and the naysayers will go quiet or change their tune.

Making change, transforming and the building the new is hard. It’s harder than you think but it’s rewarding, fun and definitely worth the effort from an organisation to put the right leadership to deliver.

Get the delivery right is critical. Sometimes it’s hard to know where to start, but once you start you’ll get the momentum to keep going.

At Whiteark, we love helping companies execute their plans. Taking the strategy and what success looks like (goals) and building a roadmap and plan that can be delivered. We coach and help businesses set up their program with test and trial and an approach that works for them. Our goal is to ensure they can execute and that the capability in the organisation is developed to own the go-forward.

Are you measuring what matters?

If it’s not part of your KPIs it’s probably not worth measuring.

Most of us have heard the phrase ‘what measures gets done’. Sounds simple right? But when it comes to measuring what matters, it gets a bit tricker

If it’s not part of your KPIs it’s probably not worth measuring.

Most of us have heard the phrase ‘what measures gets done’. Sounds simple right? But when it comes to measuring what matters, it gets a bit tricker.

There are many organisations that aren’t clear on what they should be measuring. An easy way to address this is by using my KPI scorecard – see the breakdown below.

1/ Alignment to Strategy

Ensure the metrics being measured align with your organisation’s strategy. For example, if you’re measuring organic traffic to your website but your strategy is all about driving leads via performance advertising, then this should be your first focus.

Every KPI should have a measurable lead indicator. Sure, you can measure outside of this, but put your KPI measurements first and ensure they are adequately resourced before looking at anything else.

2/ Set Targets

For each of the key metrics, set targets that are a stretch by achievable. These targets should align to a financial year; end of year target and monthly profile to deliver the end of year metric.

Look at your baseline for last fin year and then consider the environment you’re operating in now and what kind of % increase you think can realistically be achieved. Talk to the relevant experts in the business and ask them to help form a plausible growth scenario.

3/ Regular Measurement

When selecting what data outputs you’ll be measuring, get picky. There should be no more than 20 key metrics that a business reviews and measures each week. For metrics that aren’t performing; a detailed plan should be prepared for the next month to get the metric back on track.

4/ Refresh Your Metrics

Sticking to the same strategy all year isn’t always realistic. The beauty of measuring strategic outcomes each month allows for real time business decisions. This informed angle, means you can confidently pivot when necessary. If this is the case, update your metrics to align with these changes. And don’t forget to clearly document these changes and communicate them to the wider team. Especially those who are managing measurement.

TOP TIP

It’s important to note; while financial metrics are critical, non-financial metrics are also key drivers, working to align the overall vision and values of the organisation.

Stop Your Reporting

Once you’ve sorted your KPI scorecard, it’s time to take a step back. Most organisations have so much reporting that it doesn’t get reviewed or given the attention needed to make it valuable. This is a common problem and can also make the task of analysing data end up in the ‘too hard basket’.

So stop. Now that you have a clear idea of what you should be focussing on, everything else is just clutter. Put in place one weekly dashboard of the top 20 metrics that align to the business objectives. Provide performance and commentary for how each of the metrics are tracking. If you have a clear view on these, you’re much better off than measuring more but not reporting accurately.

Need a Starting Point?

Whiteark can help. We have a network of experts with practical experience implementing metrics measurements that matter to organisations. Whether it’s advice or hands-on assistance, the Whiteark team are your go-to for valuable data analysis. Contact whiteark@whiteark.com.au or 1300 240 047 to discuss.

Happy End of Financial Year.

It’s a great opportunity to reflect. What have I achieved this year. What am I most proud of. What is my biggest learning. Who has supported me this year – make sure you say thank-you. I always encourage my teams to update their CV every year – what have they learnt, where have they developed it’s a good way to remember all your achievements as well.

Happy end of Financial Year

– the clock strikes midnight on the 30th June…..Yipppppeeeeee.

I’m an accountant at heart, so 30th June is more exciting than New Years Eve. Why?

It’s a great opportunity to reflect. What have I achieved this year. What am I most proud of. What is my biggest learning. Who has supported me this year – make sure you say thank-you. I always encourage my teams to update their CV every year – what have they learnt, where have they developed it’s a good way to remember all your achievements as well.

It’s also a new beginning in some respects:

New budget

New goals / objectives

New priorities

New Funding

New Tax Year

There is an element in companies, where people need to wait until 1 July, until they can spend the money on the next project, phase or project or new recruitment. It’s kinda silly but you see how it happens as the funding aligns with the new financial year.

The new financial year, gives you a chance as a leader to reset with your team – to set them up on clear priorities, with clear goals and provide a chance for a reset, if things haven’t gone to plan in the old FY. Starting the year with clear priorities and goals is critical and defining what success is for the year for the company, department, team and individual.

Getting some momentum at the beginning of the Financial Year is critical, for people to see the pace has changed, that energises the team and resets the expectation on how the team is going to operate. Finding some quick wins at the beginning of the financial year for the team is a good focus as a leader.

Measuring what matters, makes sense. Many companies don’t do this well. Starting a new financial year allows you to reset the priorities of the company and ensuring that you are measuring lead and lag indicators – not to many metrics but the right ones. Having regular reporting with these metrics is critical and ensures changes can be made as required / and quickly to change the course of the outcomes

So why I love the end of financial year:

It’s a chance to reflect on the old year

It’s a chance to reset the ways you are doing things for the new year to make it bigger and better

It’s a change to set your team and organisation up for success

Are you ready for the new FY, the budget is approved:

Have you defined your success metrics

Have defined your reporting

Have you defined how you are going to operate

Have you engaged your team on this journey

Happy Financial Year – from the Whiteark team.

The Whiteark Guide to Strategy & Execution

THE GUIDE | The key building blocks to guide the process of strategy to execution. Answering strategic questions will form the basis of the key components to the Company Strategy building block. Constantly monitoring the industry, market and economic trends is critical for setting and achieving your strategic objectives.

The key building blocks to guide the process of strategy to execution.

Answering strategic questions will form the basis of the key components to the Company Strategy building block.

•What is your current situation?

•Where do you want to go from here?

•What do you want to accomplish?

•How do you get from where you are today to where you want to be in the future? What are the steps do you need to take?

•What obstacles will you have to overcome? What problems will you have to solve?

•What skills and capability do you require to achieve your strategic objectives?

•What problem does your company seek to solve?

•Why do you believe this problem needs to be addressed?

•Does this problem matter to others?

•What are your offerings to solve this problem?

•What is the nature of your products and services?

•What specific customer/consumer needs are you addressing?

•Who are your ideal/target customers?

•What is your unique selling proposition?

•Are there other comparable offerings in market?

•What differentiates you from your competitors?

In today’s unpredictable environment strategic planning needs to be adaptive.

Covid-19 has been the catalyst for companies to reset their business strategy. In a time of such uncertainty, executive leaders need to be increasingly reliant on adaptive strategies so that they can set long-term goals but still flex with evolving conditions.

Contents of the Guide.

Key building blocks for strategy to execution

Considerations for each building block

Adaptive strategy

Building block one - market and industry trends

Building block two - companies strategy

Building block three - build the plan

Building block four -manage performance

Looking for help with your strategy? Reach out.

Whiteark is not your average consulting firm, we have first-hand experience in delivering transformation programs for private equity and other organisations with a focus on people just as much as financial outcomes. We understand that execution is the hardest part, and so we roll our sleeves up and work with you to ensure we can deliver the required outcomes for the business. So, if you’re looking to transform, reimagine or upgrade your strategy, then give us a call on 1300 240 047 for an no-obligation conversation.

Our co-founders have a combined experience of over 50 years’ working as Executives in organisations delivering outcomes for shareholders. Reach out for a no obligation conversation on how we can help you. Contact us on whiteark@whiteark.com.au

General Insurance Australia

The industry is forecast to improve over the next five years, as local and global economies are projected to record stronger growth. Interest rates are expected to rise too, which will likely boost investment income for insurers. The industry includes general insurers and reinsurers. General insurers underwrite insurance policies to cover individuals and businesses' financial loss associated with property, casualty, liability and other risks. Underwriting involves assuming risks and assigning premiums. ]

Industry Report

General Insurance in Australia

The industry is forecast to improve over the next five years, as local and global economies are projected to record stronger growth. Interest rates are expected to rise too, which will likely boost investment income for insurers.

The industry includes general insurers and reinsurers. General insurers underwrite insurance policies to cover individuals and businesses' financial loss associated with property, casualty, liability and other risks. Underwriting involves assuming risks and assigning premiums. Reinsurers assume all or part of the risk associated with existing insurance policies underwritten by other insurers.

The occurrence of natural disasters has resulted in a rise in the number of claims, forcing industry operators to raise premiums. The COVID-19 pandemic has also led to a shift in types of insurance claims.

DEMAND DETERMINANTS

OVERALL ECONOMIC ACTIVITY | CONSUMER WEALTH | DEMOGRAPHICS | BUSINESS AND CONSUMER CONFIDENCE | RISK PROFILES | PREMIUMS

Demand for products from the General Insurance industry is affected by many factors including: overall economic activity, consumer wealth, demographics, business and consumer confidence, risk profiles and premiums. Wider economic activity affects insurance demand through exposure to risk. Higher employment leads to more risk associated with workers' compensation. A strong economy and labour market increases disposable income, driving household consumption and wealth and therefore, generates greater demand for insurance. Similarly, any decrease in overall economic activity can reduce household coverage, as wealth and consumer expenditure decline. Demographics also influence insurance demand, with individuals' coverage and expenditure increasing as they age. Premiums affect coverage levels and the volume of policies offered. Premium increases can constrain demand and reduce coverage as consumers self-insure when insurance costs outweigh potential payout gains.

OUTLOOK 2021 - 2026

Industry revenue is projected to grow over the next 5 years; driven by the anticipated economic recovery from the recession which is likely to generate demand for general insurance products, providing insurers with the opportunity to grow premium revenue. Additionally, forecasted growth in the cash rate and bond yields will enable operators to generate higher investment returns. Adversely, strong industry competition is forecast to put pressure on profit margins as well as the effects of the 2019 Royal Commission into Misconduct in the Banking, Superannuation and Financial Services which is to come into effect as at 1 July 2021.

The major players are projected to continue to dominate the industry, intensifying price competition and increasing policy coverage. Strong competition is likely to impact Small/Medium Enterprises the most. Large insurers hold more capital, so they can bear higher pricing risks and are better placed to add further coverage to existing policies. Online aggregators have driven a rise in competition, as greater price transparency has generated additional pressure on firms to compete on price.

Larger insurers have a history of aggressive expansion through M&A, and further activity is projected which is expected to reduced industry enterprise and establishment numbers. Employment numbers are also anticipated to drop marginally, as key players continue to acquire smaller operators.

External competition is likely to increase as non-traditional insurers and large technology companies, such as Google, Facebook and Amazon, are anticipated to push into the industry. These companies have been making inroads into online user experience and customisation, and have demonstrated an ability to quickly enter and disrupt new markets. However, the pandemic has forced insurers to accelerate the adoption of digital technology.

The industry will likely face some technological disruption. While technological developments could increase competition within the industry, it also creates opportunities for industry players to to expand, given the growing popularity of cloud computing and business being conducted online.

Cyber insurance is becoming an increasingly popular area of general insurance, which typically covers losses from data theft and other IT-related risks. This market remains largely untapped and presents an opportunity for operators, given the complexity and risks of the cyber landscape.

Source: IBISWorld | General Insurance in Australia, March 2021

LOOKING TO CREATE VALUE IN YOUR ORGANISATION? LET US HELP.

Whiteark is not your average consulting firm, we have first-hand experience in delivering transformation programs for private equity and other organisations with a focus on people just as much as financial outcomes. We understand that execution is the hardest part, and so we roll our sleeves up and work with you to ensure we can deliver the required outcomes for the business.

Our co-founders have a combined experience of over 50 years’ working as Executives in organisations delivering outcomes for shareholders. Reach out for a no obligation conversation on how we can help you. Contact us on whiteark@whiteark.com.au

Life's not always fair, but it's sure made me tough...

Jo Hands writes about what makes her tick, she explains “Life's not always fair, but it's sure made me tough...” When I was a child I was big about justice. I wanted to feel like life was fair. My mother told me that life wasn't fair and I thought that was crap. As I grew up I realised that she was right - life is not fair. Everyone has their challenges, battles and hard times, you are not alone. People want to be perceived as having their life together but no one really does, let's be honest.

When I was a child I was big about justice. I wanted to feel like life was fair. My mother told me that life wasn't fair and I thought that was crap. As I grew up I realised that she was right - life is not fair. Everyone has their challenges, battles and hard times, you are not alone. People want to be perceived as having their life together but no one really does, let's be honest.

The hard times is where I've learnt so much, I've grown, I've backed myself, I've realised how strong I really am. I want to make a difference to people. I love people - I love my team, people I meet, I want people to be successful and I genuinely want the best for people.

I'm good at business, it gets me out of bed in the morning with a spring. I love helping people get the most out of their business. There is so much opportunities to drive better outcomes in business - I see it and I want to help people.

Making a difference isn't easy - there are a lot of people telling you why it's not possible, it's not good enough. Experience tells me to trust my gut. Embrace and push through the change as the outcome will be better they just can't see it. I'm confident in my ability and I'll admit when I'm wrong but I will not stop striving for great.

For people that know me well, I'm an open book, someone who cares so deeply, someone who loves to make a difference and I have a genuine love of people and business optimisation.

Life isn't fair. Life isn't kind. But everyone has their journey that has shaped them and so embrace the imperfections and make the best of your life.

🙃 Smile - lean in - no regrets.

💜 Embrace life and make the best of everyday. Be kind to you - you're only human and you're enough.

🌈 Be kind - you don't know peoples journey and kindness is overrated.

Read more articles by Jo Hands:

We’re Whiteark. Leaders in Transformation & Private Equity.

Fuelled by passion, we revel in working with Private Equity; the pace, targeted focus on business optimisation and limited timeframes spark unforeseen transformation opportunities, which we’re excited to deliver on. Our approach is rooted in data, ensuring the right decisions are made – based on accurate information. Hands-on, we get into the trenches with you, working directly with the management team to realise outcomes expected by shareholders. We offer a range of transformation services which can be tailored to suit standard private equity options; always accompanied by a laser focus on profit optimisation of the business.

Reach out for a no obligation conversation on how we can help you. Contact us on whiteark@whiteark.com.au

Article by Jo Hands, Co-Founder Whiteark

How should we think about Complexity? Is it complicated?

Mark Easdown writes about complexity. In the mid 1980s, a school of thought emerged around “Complexity” and “Complex Adaptive Systems” with the formation of the Sante Fe Institute, formed in part by former members of Los Alamos National Laboratory. The institute drew from multi-disciplinary domains and insights of : economics, neural networks, physics, artificial intelligence, chaos theory, cybernetics, biology, ecology and archaeology. Theories on Complexity and Complex Adaptive systems sought to develop common frameworks and understandings of physical and social systems that was an alternate to more linear and reductionist modes of thinking.

Article written by Mark Easdown

Business Planning, Mental Models, Ways of Thinking & Working

“A complicated system is the sum of its parts. You can solve problems by breaking things down and solving them separately. In a complex system, the properties of the whole are the result of interaction between the parts and the linkages and the constraints. In fact, in a complex system how things connect is more important than what they are. So, the properties of that emergent pattern can never be decomposed to the original parts.” David Snowden

“The problem is complexity (in financial markets) …we cannot prepare for every thread of causality through every interaction; in the speed of the event we find there is no time to make adjustments.” Richard Bookstaber

“Nature likes to over-insure itself. Layers of redundancy are the central risk management property of natural systems.” Nassim Taleb

In the mid 1980s, a school of thought emerged around “Complexity” and “Complex Adaptive Systems” with the formation of the Sante Fe Institute, formed in part by former members of Los Alamos National Laboratory. The institute drew from multi-disciplinary domains and insights of : economics, neural networks, physics, artificial intelligence, chaos theory, cybernetics, biology, ecology and archaeology. Theories on Complexity and Complex Adaptive systems sought to develop common frameworks and understandings of physical and social systems that was an alternate to more linear and reductionist modes of thinking. Members sought to better understand spontaneous, self-organising dynamics and found examples in the;

Natural World - Brains, Immune Systems, Ecologies, Cells, Developing Embryos and Ant colonies

Human World – Political parties, Scientific communities and in the economy

Why bother?

Just say you and your team are facing a complicated problem, then you may break down the problem into component parts, build an expert team internally or partner with external consultants, you may take a data driven or fact-based approach, you may identify best practices create a strategic plan and solve the problem incrementally. However, is that all? Is there a one size fits all solution to problem solving?

What if your problem could be categorised with traits such as;

Levels of uncertainty, ambiguity, unpredictability, dynamic interfaces - many diverse and independent parts that were interrelated, interdependent and linked through many interconnections into a network

The properties of the whole cannot be predicted from the behaviours of the component parts, in fact the network of many components may be gathering information learning and acting in parallel in an environment produced by these interactions – the system co-evolves within its environment

There may be significant political, social or external influences

“Wise executives tailor their approach to fit the complexity of the circumstances they face.” David Snowden & Mary Boone

Where in the real world might it be useful to have sound thinking about complexity and solving problems?

In Project Management

Programs of work and problems to solve come in a variety of forms, at the simpler end of spectrum process re-engineering and best practices serve us well to achieve desired outcomes. Yet increasingly, our problems to solve are complicated, we need to analyse things to figure out what to do and cause and effect are distanced. Complex projects are harder still, they display behaviours such as self-organising, emergent properties, non-linear and phase transition behaviours. We need a different mindset, structure and strategy to wrestle with these problems.

In Financial Markets

These are complex adaptive systems, tightly coupled with unexpected feedback loops, with investors of different investment styles & horizons, the sum of the parts will not explain the whole in a linear manner, there are infrequent extreme price moves, not normally distributed.

In Nature

Complex collective behaviours are displayed when individual ants forage for food and lay down a pheromone trail on the way out from the colony and if successful finding food lay down even more on way back to the colony. Other ants follow this stronger pheromone trail to the food adding their pheromone. So, the pheromone trail becomes the whole colonies best path to food, it is an ant colony optimisation algorithm. Interestingly, this insight has helped form the basis of swarm intelligence and a wide array of solutions across routing and scheduling problems and bayesian networks.

The twenty-first century will be the "century of complexity" Stephen Hawking

COMPLEX PROGRAMS

“Strategy in complex systems must resemble strategy in board games. You develop a small and useful tree of options that is continuously revised based on the arrangement of the pieces and the actions of the opponent. It is critical to keep the number of options open. It is important to develop a theory of what kinds of options you want to have open” - John H Holland

In complex situations "cause and effect are only coherent in retrospect and do not repeat" - Sarah Sheard

Complex problems to solve are unique and they challenge some of the traditional approaches to program and risk management thinking, which may emphasise a need to identify risks in order to control them or completely plan and control programs of work. Examples of complex programs may include: computer systems and networks, buildings, bridges, planes, ships and automobiles.

Let’s take a look at what makes complex programs unique;

Sophisticated structures with many component parts interacting with each other, giving a degree of uncertainty whereby you may not know what you don’t know until it occurs

Unknowable interdependencies across domains, a need for agility and structures that favour the decentralised and local to the centralised approach.

There may be interfaces with complementary projects which present challenges in scheduling of these interconnected systems, teams and resources

The environment may have a political realm where new government decisions or public policy arises

So, what is a desirable mindset for complex programs?

A Forward focus, a willingness to proactively manage project development and critical issues through agility, collaboration and adaptability. You may need nuanced responses and local innovation.

Analysis of likely origins of complexity and thinking through dependencies, seek critical junctions, vulnerabilities & countermeasures. Contingency planning around time, buffering on sequencing, budget and people skills

Dynamic reporting and monitoring, a willingness to pick up early warning signs and take corrective actions

Communications will be dynamic, real time & high visibility (as small changes can have oversized consequences amplified by scale of some projects)

Program planning may have both a single view and multiple integrated project schedules

Cynefin is a framework to deal with predictable and unpredictable worlds (David Snowden)

In 1999, David Snowden described a framework and problem-solving tool which helps to adjust management style to fit circumstances, and has relevance across product development, marketing, organisational design and BCP/DR and crisis management. The framework had 5 domains;

OBVIOUS. Options are clear, steps to success are known, variables well known, cause-effect relationships are apparent, you are able to assess the situation, follow a procedure, categorise its type and base your response on best practice (processes & procedures) and feasible to achieve best possible result. Examples: Product mass production, cooking with a recipe, known scientific issues, known legal issues.

COMPLICATED. Solutions not obvious to everyone but most variables involved are well known, cause-effect relationships are apparent, you may assess a situation, build a diverse team or utilise experts to deliver the best response. The best that can be achieved is a good result, maybe not the best result. Examples: Existing product enhancements, coaching a team, adopting new approaches, hiring process.

COMPLEX. The context is often unpredictable, many factors uncertain, many variables may intervene, data may be incomplete, it may not be possible to determine right options, make predictions or find cause-effect relationships, there may be multiple methods to address issues. Exploring what has a proven record in past situations, small tests or business experiments, simple guidelines, brainstorming, innovation and creativity may drive solutions. Examples: weather predictions, stock markets, poker, epidemic controls.

CHAOTIC. The situation is where nobody knows what to expect, anything can happen, it is impossible to make predictions. You may have to act towards the urgent and important, then check and evaluate result before responding to that result and acting again. Examples: Innovate new products, anything which predicts people’s preferences or behaviours, crisis event and crisis management, warfare

DISORDER. The situation is not known, you need to firstly move to a known domain & gather more information.

COMPLEXITY IN FINANCIAL MARKETS

“In the last few years the concept of self-organising systems – of complex systems in which randomness and chaos seem spontaneously to evolve into unexpected order – has become an increasingly influential idea that links together researchers in many fields, from artificial intelligence to chemistry, from evolution to geology. For whatever reason, however, this movement has so far largely passed economic theory by. It is time to see how the new ideas can usefully be applied to that immensely complex, but indisputably self-organising system we call the economy” - Paul Krugman 1996

“By one estimate, 90% of international transactions were accounted for by trade before 1970, and only 10% by capital flows. Today, despite a vast increase in global trade, that ratio has been reversed, with 90% of transactions accounted for by financial flows not directly related to trade in goods and services.” - Didier Sornette 2003

“Fundamental analysis seeks to establish how underlying values are reflected in stock prices, whereas the theory of reflexivity shows how stock prices can influence underlying values. One provides a static picture, the other a dynamic one.” - George Soros

Financial markets have all the basic components of complex adaptive systems, namely:

Investors have differing investment strategies and horizons from trading at the speed of light to long term cyclical horizons. They take external information and combine it with their own strategic intent and these compete in financial markets => this is adaptive decision making

Financial markets is the aggregation of large-scale collective decision making and actions => these are developing, complex and emergent

Financial markets exist in a non-equilibrium state , are non linear, they experience non-frequent extreme price moves with the aggregate behaviour more complex than would be predicted by the sum of the individual parts.

Financial Markets are subject to feedback loops, where the result of one iteration becomes an input of next iteration

So, how has the emerging knowledge of complexity and financial markets framed regulators thinking?

The global financial crisis highlighted the complexity, leverage, inter-connected and tightly coupled of financial markets. In response we have seen;

Efforts to reduce interconnectedness (intra-day local trading halts, regional collateral exchanges)

Enhanced capital rules (increased contingency buffers and incentives for some activities to be managed by non-bank sector & efforts to reduce concentration of risks)

Enhanced liquidity rules (increase quantum and quality of contingency buffers)

Speed, agility and quantum of central bank and treasury initiatives to address market panics and crisis

A re-think of the rule-making complexity and mental models applied to finance;

“Modern finance is complex, perhaps too complex. Regulation of modern finance is complex, almost certainly too complex. That configuration spells trouble. As you do not fight fire with fire, you do not fight complexity with complexity. Because complexity generates uncertainty, not risk, it requires a regulatory response grounded in simplicity, not complexity. Delivering that would require an about-turn from the regulatory community from the path followed for the better part of the past 50 years. If a once-in-a-lifetime crisis is not able to deliver that change, it is not clear what will.” - Andrew Haldane Bank of England Speech 2012 “ The Dog and the Frisbee” [https://www.bis.org/review/r120905a.pdf ]

COMPLEXITY IN NATURE

In her TED Talk, Deborah Gordon: The emergent genius of ant colonies: highlights an example of a complex adapative system with no central control or management in an ant colony: [ https://www.youtube.com/watch?v=ukS4UjCauUs]

So, what is the strategy of the ant colony to constantly adapt to its complex environment? As per Deborah Gordon studies;

The ant colony allocates simple roles

At any given time 25% are patrolling, foraging and doing maintenance, 25% are inside with queen ant doing maintenance and looking after larvae, and finally 50% appear to be contingency and in reserve, able to surge as required to collect more food, patrol or more maintenance.

Communications are not centralised, they are dynamic, simple and local rules to adapt to emergent environment

The process is noisy, messy, imperfect and requires individual dynamic communications

Ant colonies can learn at the individual level by trial and error over many generations but this can nurture collective memory and problem-solving skills. The local instructing the central.

“So, the key to unlocking the efficiency of a leaderless system will rely on, among other things: clear role definition, flexible task allocation, a sense of responsibility toward the group, and shared understanding and response to communication patterns. Organizations would need to make an incredible investment in their employees, and vice versa.” Amanda Silver – Organising complexity – How Ant colonies self-manage. [https://medium.com/swlh/organizing-complexity-how-ant-colonies-self-manage-50455358f3cd]

How we should think about complex domains is still evolving, a multi-disciplinary lens across research and practice has been adding to this knowledge pool for decades. It is a vital enquiry for humankind, especially as our challenges become more complex to solve and our climate is as a complex adaptive system.

‘“he climate is a common good, belonging to all and meant for all. At the global level, it is a complex system linked to many of the essential conditions for human life.”- Pope Francis 2015

LOOKING TO CURATE YOUR BUSINESS STRATEGY? REACH OUT.

Whiteark is not your average consulting firm, we have first-hand experience in delivering transformation programs for private equity and other organisations with a focus on people just as much as financial outcomes.

We understand that execution is the hardest part, and so we roll our sleeves up and work with you to ensure we can deliver the required outcomes for the business. Our co-founders have a combined experience of over 50 years’ working as Executives in organisations delivering outcomes for shareholders. Reach out for a no obligation conversation on how we can help you. Contact us on whiteark@whiteark.com.au

Article written by Mark Easdown

Driving value creation

Jo Hands writes all about driving value creation. Value creation is a word that’s used a lot, but what does it mean? Creating value - customer, consumer and financial. When a company buys a business, they focus on value creation. The business case assumes that there is value to create. This value can be created by pulling either strategic or operational levers.

Value creation is a word that’s used a lot, but what does it mean? Creating value - customer, consumer and financial. When a company buys a business, they focus on value creation. The business case assumes that there is value to create.

Value can be created by pulling either strategic or operational levers:

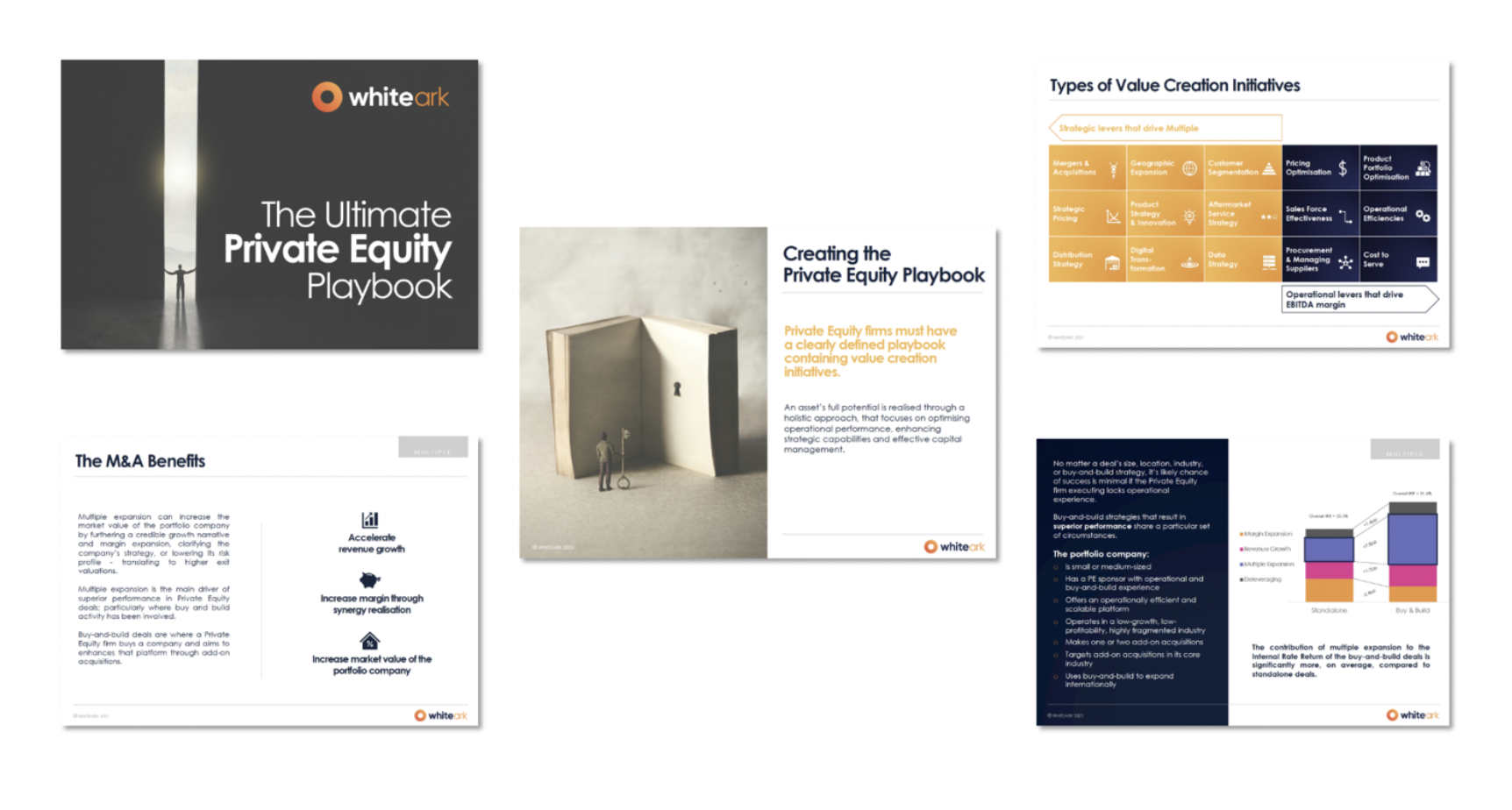

Mergers and Acquisitions: Buy-and-build deals are where a Private Equity firm buys a company and aims to enhances that platform through add-on acquisitions.

Strategic Pricing: Strategic pricing incorporates best pricing practices and ensures that your pricing strategies, analytics and processes complement your business strategy. A product’s price is based on the value to the customer, or on competitive strategy, rather than on the cost of production. By creating strategic pricing policies, analytics, and processes, you can directly capture customer value and translate to shareholder value.

Distribution Strategy: Distribution strategy is a plan to make a product or a service available to the target customers through its supply chain - to make sure the it can reach the maximum potential customers at minimal or optimal distribution costs. A good distribution strategy can maximise your revenue and profits.

Geographic Expansion: With access to new markets, a business has the potential to build a new customer base.

Product Strategy: A product strategy outlines the desired outcomes to be achieved by the product including the end-to-end vision, and how it supports the company’s strategic objectives. The product strategy is brought to life through the product road map and can be used to support any tactical decisions that the company needs to make.

Product Innovation: Product innovation represents a new way of solving a problem a high number of consumers have:

There are no products on the market that address the problem statement - unexplored market spaces could potentially generate high profits or;

There may be other products on the market that address the problem but in a different way to your innovative solution

Digital Transformation: Digital transformation is the use of technology — software enabled, connected, transactions, and interactions, across all areas of a business. The goal of digital transformation is disrupting existing business models, improving customer experience, and creating operational efficiency to drive economic value creation.

Customer Segmentation: the benefits of customer segmentation include focus, competitiveness, expansion, retention, communications effectiveness and profitability.

Aftermarket Service Strategy: The concept of aftermarket service is as important as sales, the saying “it takes years to build a reputation but just moments to ruin it” addresses the importance of keeping a customer happy and satisfied. Aftermarket service does not generate any revenue for the company, but it increases the goodwill in the market and amongst the customers.

Data Strategy: Data strategy is a central, integrated concept that articulates how data will enable and inspire business strategy.

Pricing Optimisation: Price optimisation is the practice of using data from customers and the market to find the most effective price point for a product or service that maximizes value for customers and sales or profit for the company.

Sales Force Effectiveness: Sales force effectiveness is driven by the decisions, processes, systems and programmes that sales leaders are accountable. By managing sales force effectiveness drivers, companies can build high-quality sales teams that better meet customer needs, increase productivity and successful conversion, and consequently result in improved turnover and EBITDA margins.

Procurement & Managing Suppliers: Smart procurement practices are fundamental for companies across all industries to optimise operational efficiencies and improving EBITDA margin.

Product Portfolio Optimisation: Product portfolio optimisation helps managers assess their products’ current level of success - it provides a centralized view of an entire suite of products against the prevailing marketplace for those products. Effective product portfolio optimisation highlights future opportunities for improved resource allocation, greater returns, growth and profit, and reveals products that are generating a negative contribution.

Operational Efficiencies: Operational efficiency refers to a company’s ability to reduce waste in time, effort and materials as much as possible, while still producing a high-quality service or product. Financially, operational efficiency is the ratio between the input required to keep the company going and the output it provides. When improving operational efficiency, the output to input ratio improves. The greater the operational efficiency, the more profitable a company becomes as it can generate greater income or returns for the same or lower cost.

Cost to Serve: Cost to Serve focuses on aggregate analyses around a blend of cost drivers. The analysis exposes the variation in customer demands for different activities and has a different cost profile. Without understanding the cost to serve a customer, a company is unable to determine the value that customer is contributing to their business.

The value levers are a great way of prioritising what's important.

The levers that drive the biggest value result in an improved performance that leads to greater valuation.

If you are:

1. Getting your business ready for sale

Executing initiatives that drive value and can be in the run rate results will result in a higher sale price

2. Buying a business.

Your investment case is critical to drive the appropriate acquisition price. This will also drive what transformation program looks like once the business has been bought to ensure the business case is achieved/exceeded

3. Running your own business.

Driving value is what you do everyday but sometimes it's easy to miss the levers to pull to achieve the greatest success.

At any point of a business lifecycle it's imperative that driving value is something you focus on to drive consistent and stable earnings with a positive trend.

Article by Jo Hands, Co-Founder Whiteark

Looking for more support? Download our Private Equity Playbook for the ultimate guide to value creation.

Looking to create value in your organisation? Let us help.

Whiteark is not your average consulting firm, we have first-hand experience in delivering transformation programs for private equity and other organisations with a focus on people just as much as financial outcomes. We understand that execution is the hardest part, and so we roll our sleeves up and work with you to ensure we can deliver the required outcomes for the business.

Our co-founders have a combined experience of over 50 years’ working as Executives in organisations delivering outcomes for shareholders. Reach out for a no obligation conversation on how we can help you. Contact us on whiteark@whiteark.com.au