Why I love working with Private Equity?

Over the last 10 years I have worked with Private Equity, in a CFO role, interim CFO role & through Private Equity firms as a consultant.

I love working with private equity, I’ll give you 5 reasons why.

Over the last 10 years I have worked with Private Equity, in a CFO role, interim CFO role & through Private Equity firms as a consultant.

I love working with private equity, I’ll give you 5 reasons why.

1. Fast paced – private equities have made an investment, and they want a return. Speed is the name of the game. Spending money to accelerate a project / return is justified as getting to exit with the required valuation as early as possible is the name of the game. I like this.

Spend money to save time, is a great strategy when you work with Private Equity. With private equity you need to put your runners on, red ones so you can run. Long hours, quick turnarounds & a team environment to drive an outcome in a short period of time.

2. Results oriented – private equity care about results. Whether it’s revenue, EBITDA or cash or all three they want results and they will incentive management to deliver. The incentives offered by private equity firms to deliver a financial outcome are part of the DNA. If you are an ambitious business leader, you can make some money driving very hard for private equity.

I love being results / outcome driven, it’s the way businesses should be. It’s not about the presentation packs, it's about what financial outcomes you delivered.

3. You know where you stand – honest, direct feedback from private equity means you know where you stand. If you are not performing, you won’t work there anymore. So don’t worry about what they think and continue to deliver the results at the speed.

4. Know your numbers – the PE firm expects the CFO to know the numbers, all the key numbers and be able to speak to the why behind the results. This means you need a strong team behind you that will deliver and ensure you can run along at the strategic level and ensure you also know the detail.

5. Cash is king – It wasn’t until I worked in Private Equity that I understood cash. When you report cash daily and do a 13-week cashflow forecast you start to realise that understanding all the timings and levers of cashflow is critical and while the Income statement is critical, knowing cashflow and how to pull the levers becomes critical.

What you learn is that cashflow doesn’t lie. Understanding earnings to cashflow means you can really understand where you are leaking cash.

Not every Private Equity firm is the same, so this article is a generalisation however it gives you a flavour and feel on the 5 key reasons I love Private Equity

At Whiteark we provide a number of services to Private Equity portfolio companies:

👉 Transition work

👉 Integration work

👉 Transaction work

👉 CFO transformation and operating model

👉 Transformation work

Led by Jo Hands who has experienced, capable, hands-on professionals who have done this before and want to help your team and business too.

We have a number of publications that you might find interesting:

Our work at Whiteark is focused on value creation levers, we have case studies for each of these levers that you can see on our website: https://www.whiteark.com.au/

We also have a number of articles that are relevant around private equity.

You might want to explore other thought leadership articles

Driving value creation

Jo Hands writes all about driving value creation. Value creation is a word that’s used a lot, but what does it mean? Creating value - customer, consumer and financial. When a company buys a business, they focus on value creation. The business case assumes that there is value to create. This value can be created by pulling either strategic or operational levers.

Value creation is a word that’s used a lot, but what does it mean? Creating value - customer, consumer and financial. When a company buys a business, they focus on value creation. The business case assumes that there is value to create.

Value can be created by pulling either strategic or operational levers:

Mergers and Acquisitions: Buy-and-build deals are where a Private Equity firm buys a company and aims to enhances that platform through add-on acquisitions.

Strategic Pricing: Strategic pricing incorporates best pricing practices and ensures that your pricing strategies, analytics and processes complement your business strategy. A product’s price is based on the value to the customer, or on competitive strategy, rather than on the cost of production. By creating strategic pricing policies, analytics, and processes, you can directly capture customer value and translate to shareholder value.

Distribution Strategy: Distribution strategy is a plan to make a product or a service available to the target customers through its supply chain - to make sure the it can reach the maximum potential customers at minimal or optimal distribution costs. A good distribution strategy can maximise your revenue and profits.

Geographic Expansion: With access to new markets, a business has the potential to build a new customer base.

Product Strategy: A product strategy outlines the desired outcomes to be achieved by the product including the end-to-end vision, and how it supports the company’s strategic objectives. The product strategy is brought to life through the product road map and can be used to support any tactical decisions that the company needs to make.

Product Innovation: Product innovation represents a new way of solving a problem a high number of consumers have:

There are no products on the market that address the problem statement - unexplored market spaces could potentially generate high profits or;

There may be other products on the market that address the problem but in a different way to your innovative solution

Digital Transformation: Digital transformation is the use of technology — software enabled, connected, transactions, and interactions, across all areas of a business. The goal of digital transformation is disrupting existing business models, improving customer experience, and creating operational efficiency to drive economic value creation.

Customer Segmentation: the benefits of customer segmentation include focus, competitiveness, expansion, retention, communications effectiveness and profitability.

Aftermarket Service Strategy: The concept of aftermarket service is as important as sales, the saying “it takes years to build a reputation but just moments to ruin it” addresses the importance of keeping a customer happy and satisfied. Aftermarket service does not generate any revenue for the company, but it increases the goodwill in the market and amongst the customers.

Data Strategy: Data strategy is a central, integrated concept that articulates how data will enable and inspire business strategy.

Pricing Optimisation: Price optimisation is the practice of using data from customers and the market to find the most effective price point for a product or service that maximizes value for customers and sales or profit for the company.

Sales Force Effectiveness: Sales force effectiveness is driven by the decisions, processes, systems and programmes that sales leaders are accountable. By managing sales force effectiveness drivers, companies can build high-quality sales teams that better meet customer needs, increase productivity and successful conversion, and consequently result in improved turnover and EBITDA margins.

Procurement & Managing Suppliers: Smart procurement practices are fundamental for companies across all industries to optimise operational efficiencies and improving EBITDA margin.

Product Portfolio Optimisation: Product portfolio optimisation helps managers assess their products’ current level of success - it provides a centralized view of an entire suite of products against the prevailing marketplace for those products. Effective product portfolio optimisation highlights future opportunities for improved resource allocation, greater returns, growth and profit, and reveals products that are generating a negative contribution.

Operational Efficiencies: Operational efficiency refers to a company’s ability to reduce waste in time, effort and materials as much as possible, while still producing a high-quality service or product. Financially, operational efficiency is the ratio between the input required to keep the company going and the output it provides. When improving operational efficiency, the output to input ratio improves. The greater the operational efficiency, the more profitable a company becomes as it can generate greater income or returns for the same or lower cost.

Cost to Serve: Cost to Serve focuses on aggregate analyses around a blend of cost drivers. The analysis exposes the variation in customer demands for different activities and has a different cost profile. Without understanding the cost to serve a customer, a company is unable to determine the value that customer is contributing to their business.

The value levers are a great way of prioritising what's important.

The levers that drive the biggest value result in an improved performance that leads to greater valuation.

If you are:

1. Getting your business ready for sale

Executing initiatives that drive value and can be in the run rate results will result in a higher sale price

2. Buying a business.

Your investment case is critical to drive the appropriate acquisition price. This will also drive what transformation program looks like once the business has been bought to ensure the business case is achieved/exceeded

3. Running your own business.

Driving value is what you do everyday but sometimes it's easy to miss the levers to pull to achieve the greatest success.

At any point of a business lifecycle it's imperative that driving value is something you focus on to drive consistent and stable earnings with a positive trend.

Article by Jo Hands, Co-Founder Whiteark

Looking for more support? Download our Private Equity Playbook for the ultimate guide to value creation.

Looking to create value in your organisation? Let us help.

Whiteark is not your average consulting firm, we have first-hand experience in delivering transformation programs for private equity and other organisations with a focus on people just as much as financial outcomes. We understand that execution is the hardest part, and so we roll our sleeves up and work with you to ensure we can deliver the required outcomes for the business.

Our co-founders have a combined experience of over 50 years’ working as Executives in organisations delivering outcomes for shareholders. Reach out for a no obligation conversation on how we can help you. Contact us on whiteark@whiteark.com.au

Are you making money?

Jo Hands asks the question - are you making money? It's a very simple question. Forget accounting standards and rubbish reasons your results look crap are you making sustainable earnings in your business. If your wondering how to know, here are a couple of tips…

It's a very simple question. Are you making money? Forget accounting standards and the rubbish reasons your results look crap… Be frank. Are you making sustainable earnings in your business?

If you’re wondering how to know, here are a couple of tips:

1. Cash doesn't lie - if you are cashflow positive, you are making money.

2. Majority of your costs are variable - therefore are aligned with revenue.

3. Your pricing covers your fixed and variable costs.

Now, regardless if you are making money or not - the next question is could you make more? In most cases the answer is yes. So how do you do this?

Increase revenue

increase price

more effective salesforce

more effective marketing

Reduce costs

look at ROI on all costs

review fixed costs to make variable

review operating model

Drive improved working capital

credit terms reduce to increased cashflow

use pcards to pay suppliers

improve process to reduce time to receive cashflow

There are many levers to increase profitability of your business. That's what we do at Whiteark.

See some example case studies here.

Need support in your organisation? Reach out.

Whiteark is not your average consulting firm, we have first-hand experience in delivering transformation programs for private equity and other organisations with a focus on people just as much as financial outcomes.

We understand that execution is the hardest part, and so we roll our sleeves up and work with you to ensure we can deliver the required outcomes for the business. Our co-founders have a combined experience of over 50 years’ working as Executives in organisations delivering outcomes for shareholders. Reach out for a no obligation conversation on how we can help you. Contact us on whiteark@whiteark.com.au

Article by Jo Hands, Co-Founder Whiteark

How to deliver a successful transformation program

Jo Hands writes about how to deliver a successful transformation program. Nearly every project today is called a transformation. Most companies are changing, evolving and putting in programs to change the way things are done and these call these programs – ‘transformation project’s. It doesn’t matter what the programs are called, what matters is the that it achieves the outcome you are expecting.

Nearly every project today is called a transformation. Most companies are changing, evolving and putting in programs to change the way things are done and these call these programs – ‘transformation project’s. It doesn’t matter what the programs are called, what matters is the that it achieves the outcome you are expecting.

The statistics are terrible, however on average 20% of transformation programs achieve the required outcomes, this is a terrible statistic. Many companies put money, focus and effort into delivering the outcome however they are unable to deliver the required outcome.

Why?

There are four main reasons that transformation programs are not successful:

Success for the project has not been defined and is not well understood. Being very clear on what the project is trying to achieve, what is success and how the results are going to be measured is critical.

No Executive sponsorship – the Executive team do not sponsor the project and help show how important it is.

No accountability for the outcomes. The roles & responsibilities are not clear and the people running the program are not being held accountable and this flows down.

The organisation doesn’t want the change/they haven’t bought in and they make it so hard that the organisation gives up. It’s all too hard.

Once one or all of the 4 above happen the transformation program will likely not be successful, will not deliver the required outcome and next time people try they will say we tried this and it doesn’t work in our company.

No one sets out for it not be successful so how to do maximise the chance of success for your transformation program. There are four main things that will help maximise success:

Be very clear on what success is – define success, work out how to measure success & ensure you communicate this change to people impacted and key stakeholders

Ensure you have an Executive Sponsor that will support and drive the project and help clear blockages that are in the way

Build a change champion network in the organisation – key people that can champion change and support the program

Demonstrate progress and the ‘what is in it for me’ mentality to show people why change can be great

The success of transformation will be driven from the ability of the lead:

To set up the program for success

To get buy in

To not listen to naysayers

To focus on delivering outcomes and communicating

To build out the what is in it for me

The lead for the transformation needs to be very strong leaders, someone who is not worried or concerned about driving change and showing resilience.

From experience, I have seen many transformations go really well. I am someone who doesn’t like to give up and I like to be on the winning team – everyone makes mistakes and from these comes learnings and experience that helps you when you do your next program/project/transformation.

At Whiteark we love helping our clients with transformation; focused on ensuring that we can use our experience to help ensure their transformations are successful. If you are interested in having a conversation about how we can help you, reach out.

Need support in your transformation project? Reach out.

Whiteark is not your average consulting firm, we have first-hand experience in delivering transformation programs for private equity and other organisations with a focus on people just as much as financial outcomes.

We understand that execution is the hardest part, and so we roll our sleeves up and work with you to ensure we can deliver the required outcomes for the business. Our co-founders have a combined experience of over 50 years’ working as Executives in organisations delivering outcomes for shareholders. Reach out for a no obligation conversation on how we can help you. Contact us on whiteark@whiteark.com.au

Article by Jo Hands, Co-Founder Whiteark

M&A Trends and Insights

The economic impact of COVID-19 has led to a material decline in M&A activity globally, including Australia. As a result, we have seen fewer transactions and according to Refinitiv (formerly Thomson Reuters), worldwide M&A activity totaled US$1.2 trillion during H1 of 2020, a drop of 41% compared to a year ago and the slowest opening six-month period since 2013. M&A activity abroad appears to have rebounded to some degree since the end of June 2020, presumably as economies have started to reopen.

The economic impact of COVID-19 has led to a material decline in M&A activity globally including Australia. As a result, we have seen fewer transactions and according to Refinitiv (formerly Thomson Reuters), worldwide M&A activity totaled US$1.2 trillion during H1 of 2020, a drop of 41% compared to a year ago and the slowest opening six-month period since 2013. M&A activity abroad appears to have rebounded to some degree since the end of June 2020, presumably as economies have started to reopen. The Financial Times reported that since the end of June, 8 deals each worth more than US$10 billion have been announced.

Australian Private Equity History

Compared to the US and UK private equity (PE) markets, the Australian PE market is relatively immature. The first venture capital fund was established in the mid-1980s by Bill Ferris, and the fund performed well but it was not until the Australian Government set up an Innovation Fund in the mid-1990s offering A$2 funding for every A$1 raised that the venture capital industry accelerated.

Between 2000 and 2010, deal sizes and fund sizes grew exponentially in Australia and many global private equity players such as KKR, Carlyle, TPG and Blackstone opened offices in Australia with a view to acquiring large businesses beyond the reach of the smaller newly formed local funds.

Australian Private Equity Landscape

Fundraising in Australia has become global with Australian institutions seeking global exposure and Australian PE managers having to raise funds abroad in competition with fund managers across the globe. Consequently, only the best performing funds have raised new and larger funds in Australia, while only a small number of Australian fund managers from the early 2000s are still active.

A decade ago, the vast majority of PE deals in Australia were by Australian managers investing Australian institutional money. By 2019, between 60-70 % of PE investment in Australia came from offshore funds with many adopting the “fly in fly out” model investing from their home base or from regional APAC offices in Hong Kong or Singapore. This trend for increased investment by offshore PE in Australia is set to continue for a number of reasons including:

Higher levels of local competition and high prices in their home markets of US and Europe, some growth capital funds, and buyout funds, have abroad for investments;

Australia has a stable political environment, first rate governance and rule of law, a strong economy and a reputation for technology and innovation;

Australia has reduced competition from local funds due to consolidation and the relative weakness of the Australian dollar to the US dollar, it is easy to see why Australian deal values have been attractive to US investors.

Australian M&A Market

In Australia, M&A activity for the first half was subdued. Announced deals in Australia and New Zealand dropped 51% in value terms with the largest public company transactions being:

Iberdrola’s bid for Infigen at $1.5 billion (topping an earlier bid by UAC Energy, a joint venture between AC Energy and UPC Renewables);

Uniti Group’s proposed merger with OptiComm, valued at $540m;

Shandong Gold Mining’s bid for Cardinal Resources, valued at $335m.

All other deals announced in that period had a lower value, though this excludes a number of significant transactions including:

Bain Capital’s acquisition of Virgin Australia (in administration), agreed in June, but not strictly a public company transaction, given the nature of the transaction;

TPG’s $15 billion merger with Vodafone which completed in July, as that was announced in 2018;

BGH’s $542m recommended bid for Village Roadshow as it was agreed in August.

“CONTENTS

> Introduction

> Australian PE History

> Australian Private Equity Landscape

> Australian M&A Market

> Recent Market Developments - Revised Foreign Investment Rules

> Impact of COVID on Asset Valuations - Digital and Technology assets

> Variable Consideration as part of Asset Valuation

> Renegotiation and Reneging on Agreed Transactions

Key insights from the 2H of 2020

> Deal makers widen assessment of value creation to non-traditional sources

> The impact of a hot IPO market on M&A

> Looking ahead: Resilience and innovation”

Need support with your M&A? Reach out to the Whiteark team.

We’re a team of doers led by Jo Hands and James Ciuffetelli. We don’t believe in unnecessary layers; and between us we have over 50 years of collective experience, expertise and global connections. Delicately weaving these together, we engage with you directly, with a single-minded focus on the task at hand. Collaborating at a senior level to propel organisations forward, we intricately map out and execute your next move, ensuring you’re prepared, protected and prosperous.

Fuelled by passion, we revel in working with Private Equity; the pace, targeted focus on business optimisation and limited timeframes spark unforeseen transformation opportunities, which we’re excited to deliver on. Our approach is rooted in data, ensuring the right decisions are made – based on accurate information. Hands-on, we get into the trenches with you, working directly with the management team to realise outcomes expected by shareholders. We offer a range of transformation services which can be tailored to suit standard private equity options; always accompanied by a laser focus on profit optimisation of the business.

The Ultimate Private Equity Playbook

Private Equity firms must have a clearly defined playbook containing value creation initiatives in order to succeed. This 40+ page playbook by Whiteark is the ultimate guide to realising value in your Private Equity transaction. An asset’s full potential is realised through a holistic approach, that focuses on optimising operational performance, enhancing strategic capabilities and effective capital management.

Private Equity firms must have a clearly defined playbook containing value creation initiatives in order to succeed. This 40+ page playbook by Whiteark is the ultimate guide to realising value in your Private Equity transaction.

An asset’s full potential is realised through a holistic approach, that focuses on optimising operational performance, enhancing strategic capabilities and effective capital management.

Playbook Inclusions:

✔️Overview

✔️Strategic Levers

✔️Operational Levers

✔️Identify Value Creation Initiatives

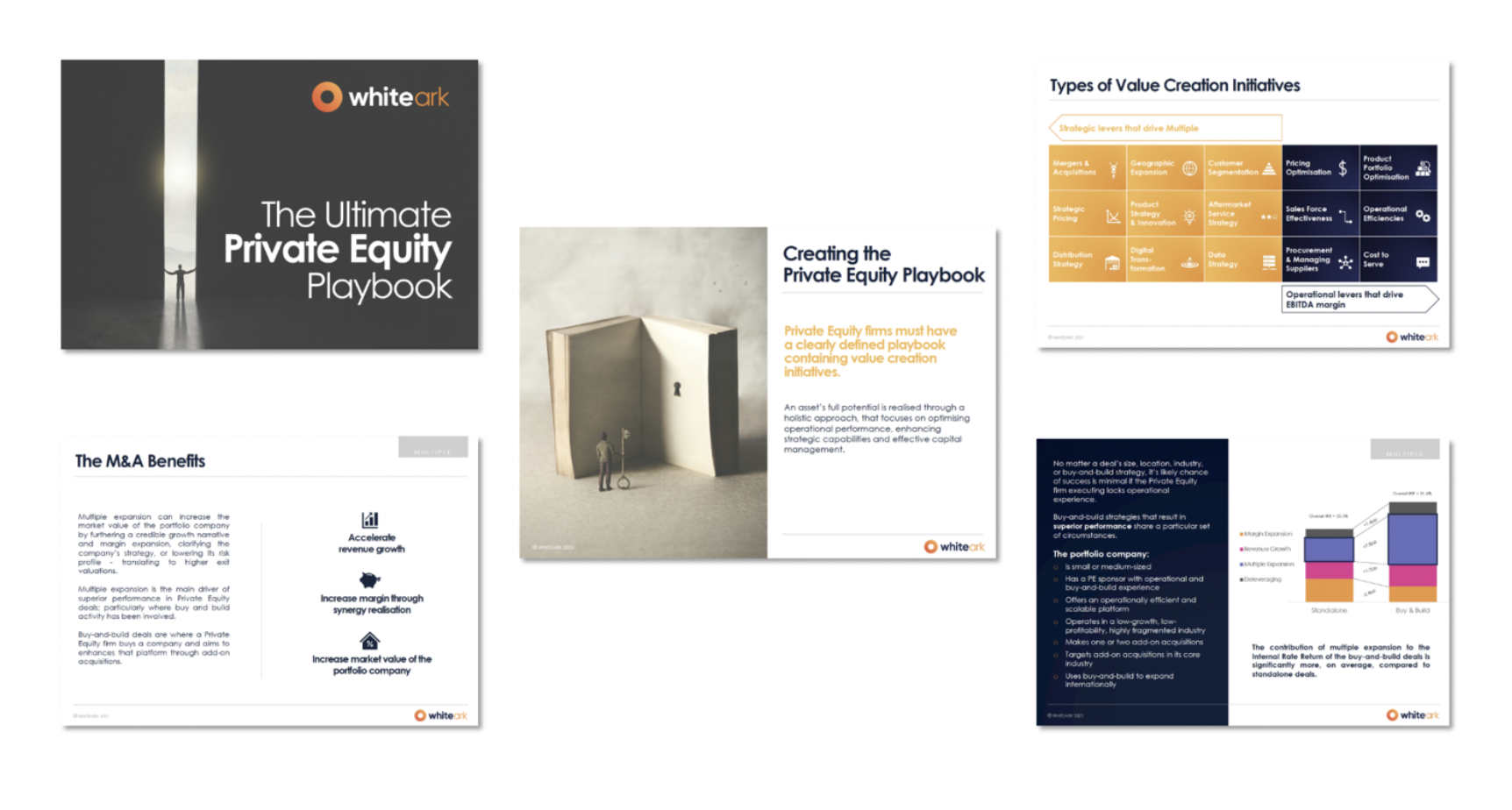

✔️Types of Value Creation Initiatives

✔️The M&A Benefits

✔️Strategic Pricing

✔️A Sharp Focus - where to target your efforts

✔️Distribution Strategy

✔️Types of Distribution Strategy

✔️Geographic Expansion

✔️Geographic Considerations: Entry to new markets, New sales, Access to local talent, Increased business growth, Competitive advantage, Operational efficiencies

✔️Product Strategy: Product Vision, Goals, Product Initiatives

✔️Product Innovation

✔️Digital Transformation Approach

✔️Digital Transformation

✔️Digital Strategy

✔️Customer Segmentation

✔️Aftermarket Service Strategy

✔️Data Strategy

✔️Data Strategy Principles

✔️Pricing Optimisation

✔️Approach to Pricing Optimisation

✔️Sales Force Effectiveness

✔️Procurement & Managing Suppliers

✔️Successful Procurement Management

✔️Pricing Optimisation

✔️Benefits of Product Portfolio

✔️Operational Efficiencies Focus Areas

✔️Cost to Serve

And more…

Get your hands on the PE playbook

Want your copy of our 40-page Private Equity playbook? Click the button below to proceed.

Private Equity is our thing. Qualified, experienced, and connected, our team is on hand to help you exceed all expectations.

With extensive experience working with private equity firms, we have the ability to drive true value in portfolio investments. Globally, and locally, our team’s combined experience bridges the gap and fills in the blanks, so we’re ready to help - exactly when you need it.

Our approach is rooted in data, ensuring the right decisions are made – based on accurate information. Hands-on, we get into the trenches with you, working directly with the management team to realise outcomes expected by shareholders. We offer a range of transformation services which can be tailored to suit standard private equity options; always accompanied by a laser focus on profit optimisation of the business.

Public M&A Activity in Australia

Public M&A activity reduced in FY20, largely due to global uncertainty and economic impacts resulting from the coronavirus pandemic. The transactions accounted for in this document involve Australian ASX listed targets that were conducted (or announced as intended to be conducted) by way of takeover bid or scheme of arrangement in FY20.

Public M&A activity reduced in FY20, largely due to global uncertainty and economic impacts resulting from the coronavirus pandemic. The transactions accounted for in this document involve Australian ASX listed targets that were conducted (or announced as intended to be conducted) by way of takeover bid or scheme of arrangement in FY20.

Source: Australian Public M&A Report 2020, Herbert Smith Freehills

TOTAL DEAL VALUE: $13.4bn

FY19 was $45.9bn / (FY15-FY19 average: $36.1bn)

ANNOUNCED DEALS: 51

FY19 was 63 / (FY15-FY19 average: 57)

SUCCESS RATE: 63%

FY19 was 74% / (FY15-FY19 average: 71%)

MEGA DEALS >$1bn: 2

FY19 was 8 / (FY15-FY19 average: 7)

DEALS INVOLVE A PRIVATE EQUITY BIDDER: 29%

FY19 was 21% / (FY15-FY19 average: 17%)

FOREIGN BIDDERS BY VALUE: 60%

FY19 was 80% / (FY15-FY19 average: 65%)

UNSOLICITED TAKEOVER BIDS: 29%

FY19 was 62% / (FY15-FY19 average: 37%)

MEDIAN TARGET VALUE: $124m

FY19 was $109m / (FY15-FY19 average: $102.1m)

The significant reduction in total deal value ($13.4bn) relative to the number of deals (51) highlights the absence of mega deals (>$1bn), with only 2 mega deals announced - the lowest recorded in 12 years.

Private equity emerged as a keen capital provider, with the ability to look beyond the pandemic in making investment decisions.

There was a steep incline in the number of deals announced in the second half of FY20 -- prior to January 2020, 18% of deals were unsolicited and post January 2020, 43% of deals were unsolicited.

Cash has re-emerged as the preferred form of consideration, with 74% of all deals offering shareholders only cash (66%) or a choice of cash (8%) as consideration. Deals were more likely to succeed if cash was offered as a consideration.

LOCATION OF TARGETS PER STATE

VALUE OF DEALS PER SECTOR

10 LARGEST ANNOUNCED DEALS

Looking for some help with M&A? We’re your people.

Whiteark is highly experienced in providing services to Private Equity firms and has had great success at driving an improvement in returns through involvement in portfolio transition and transformation projects. We understand that execution is the hardest part, and we roll our sleeves up and work with you to ensure we can deliver the required outcomes for the business. Contact us on whiteark@whiteark.com.au

A clearly defined playbook with value creation initiatives is critical for Private Equity firms

Revenue contribution to the Private Equity industry in Australia is forecast to decline 3.5% in 2020-21 due to Covid-19 disruptions, however, it is expected to grow 2.6% over the years through to 2025-26 to $725.3M. Private Equity firms need to consider the following four actions to ensure they can add value.

Revenue contribution to the Private Equity industry in Australia is forecast to decline 3.5% in 2020-21 due to Covid-19 disruptions, however, it is expected to grow 2.6% over the years through to 2025-26 to $725.3M.

Private Equity firms need to consider the following four actions to ensure they can add value to individual companies, outperform the market, and become an organisation that can confidently generate attractive returns:

Articulate a new, clear value proposition either through specialisation or economies of scale.

Achieve excellence in talent, governance, and organization.

Refine how to successfully originate and execute on deals.

Prepare for successful exits at least 18 months prior to a planned exit; allowing time for asset owners to shape a compelling equity story.

The pressure for Private Equity firms to achieve profitable returns is critical, even more so in today’s economic environment. In order to be certain they can achieve consistent returns in the fund they must focus on purchasing the investment at the right price and focusing on accelerating value creation initiatives to ensure that they can sell at a significant increase in multiple.

Private Equity firms must have a clearly defined playbook which contains value creation initiatives to support the investment thesis. This provides an advantage in knowing what to pay and the level of risk. The playbook should be refreshed and prioritised for each investment.

An asset’s full potential is realised through a holistic approach that optimising operational performance, enhancing strategic capabilities and effective capital management. The efficient use of capital is also a critical component of valuing an asset’s full potential. Capital deployment is an important foundation to support strategic and operational initiatives.

Strategic Levers

Drive Multiple

Transforms the Business Model

Mergers and acquisition

Geographic expansion

Customer segmentation

Strategic pricing

Product strategy and innovation

Aftermarket/service strategy

Distribution strategy

Digital transformation

Data strategy

Operational Levers

Drivers EBITDA Margin

Transforms Execution of the Business Model

Pricing optimisation

Sales force effectiveness

Product portfolio optimisation

Operational efficiencies through optimisation – manufacturing, distribution

Cost to serve

The business world is changing with the rapid evolution in technology, and in order for Private Equity firms to maximise the returns on their investment funds, a value creation focus in digital transformation is important.

The goal of digital transformation is disrupting existing business models, improving customer experience, and creating operational efficiency.

Strategic acquirers are more likely to pay higher multiples for successfully digitised companies, given that they are easier and faster to analyse and integrate.

Looking to create your own playbook? Let us help.

Whiteark is highly experienced in providing services to Private Equity firms and has had great success at driving an improvement in returns through involvement in portfolio transition and transformation projects. We understand that execution is the hardest part, and we roll our sleeves up and work with you to ensure we can deliver the required outcomes for the business. Contact us on whiteark@whiteark.com.au

The CFO role has never been so important. Companies are navigating uncertain territory and having a strong CFO that can manage the nuts and bolts of finance and help navigate the commercial as well is instrumental to how companies navigate this period.