How do I help my team to be more effective?

As a leader, one of your primary responsibilities is to help your team be as effective as possible.

There are a variety of strategies you can use to support your team's productivity and performance.

Here are five key ways to help your team be more effective:

As a leader, one of your primary responsibilities is to help your

team be as effective as possible. regardless of its size or industry.

There are a variety of strategies you can use to support your team's productivity and performance.

Here are five key ways to help your team be more effective:

1. Set clear goals and expectations: Clear goals and expectations are essential for helping your team stay focused and on track. Make sure everyone on your team understands what they are working toward and what is expected of them.

Clearly define key performance indicators (KPIs) and regularly communicate progress toward these goals.

2. Foster open communication: Effective communication is critical for any team to succeed. Encourage your team to share ideas and perspectives and create a safe environment for open and honest communication. Make sure everyone on the team understands the importance of communication and feels comfortable raising concerns or asking questions.

3. Provide the necessary resources: Your team needs the tools, resources, and support necessary to be effective. Make sure everyone has access to the tools and technology they need to do their jobs and provide training and development opportunities to help your team build the skills they need to succeed.

4. Empower your team: Empowering your team means giving them the autonomy and authority to make decisions and take action. This can help boost motivation and engagement, as team members feel more invested in their work and the outcomes they achieve. Trust your team to make decisions and take responsibility for their work.

5. Celebrate successes and learn from failures: Celebrate your team's successes and acknowledge their hard work and accomplishments. At the same time, don't shy away from failure. Use failures as opportunities for learning and growth and encourage your team to take risks and try new things.

In conclusion, there are many ways to help your team be more effective, including setting clear goals and expectations, fostering open communication, providing necessary resources, empowering your team and celebrating successes and learning from failures.

As a leader, your role is to support your team and help them achieve their goals. By focusing on these key strategies, you can help your team become more productive, engaged, and successful.

Check more good stuff from our thought articles library

Top 5 tips to help companies execute

Executing successfully can be a challenging task for any company, regardless of its size or industry.

However, there are certain tips that can help companies improve their execution and achieve their goals more effectively.

Executing successfully can be a challenging task for any company, regardless of its size or industry.

However, there are certain tips that can help companies improve their execution and achieve their goals more effectively.

Here are the top 5 tips to help companies execute successfully:

1. Set clear goals and priorities: A company should set clear goals and priorities that align with its vision, mission, and values. The goals should be specific, measurable, achievable, relevant, and time bound. By setting clear goals and priorities, a company can focus its efforts on what is most important and avoid distractions.

2. Communicate effectively: Effective communication is essential for successful execution. A company should communicate its goals, priorities, expectations, and progress to its employees regularly. The communication should be clear, concise, and timely. A company should also encourage open communication and feedback from its employees.

3. Build a strong team: A company should build a strong team with the necessary skills, knowledge, and experience to execute its goals successfully. The team members should be aligned with the company's vision, mission, and values. A company should also foster a culture of collaboration, innovation, and continuous learning.

4. Develop a solid execution plan: A company should develop a solid execution plan that outlines the tasks, timelines, resources, and responsibilities required to achieve its goals. The plan should be flexible enough to accommodate changes, but also structured enough to ensure accountability and progress tracking.

5. Measure and analyse progress: A company should measure and analyze its progress regularly to ensure that it is on track to achieving its goals. It should establish key performance indicators (KPIs) that are aligned with its goals and track them consistently. A company should also analyze the data to identify areas for improvement and adjust its execution plan accordingly.

In conclusion, executing successfully requires a combination of clear goals, effective communication, a strong team, a solid execution plan, and progress measurement and analysis. By following these top 5 tips, companies can improve their execution and achieve their goals more effectively.

Check more good stuff from our thought articles library

My love-hate relationship with marketing

I’m an accountant, so I am not supposed to love marketing, am I?

When I started in industry, marketing budget were cut, how can you justify the ROI on that spend. So much time was spent understanding the return on money spent, some easier than others to explain.

However, when cash needed to be saved it was the easiest spot. It didn’t impact the bottom line, that you can really measure easy compared with other costs.

I’m an accountant, so I am not supposed to love marketing, am I?

When I started in industry, marketing budget were cut, how can you justify the ROI on that spend. So much time was spent understanding the return on money spent, some easier than others to explain.

However, when cash needed to be saved it was the easiest spot. It didn’t impact the bottom line, that you can really measure easy compared with other costs.

Then I started my own business, and everything change. Marketing costs started getting put into different buckets;

• Brand – brand awareness. Wanting people to know the Whiteark brand, without awareness people will not think Whiteark when they have a problem. So, with a new business this required a bit of planning, spending and time to get right.

• Events – client events, potential client events & dinner to entertain people was important to build deeper relationships with the right network.

• Content – With the brand in play, having relevant content across social media so potential clients would spot us, understand our value proposition and when a problem came up they would think call Whiteark. Regular content and varied content that was unique was important.

• Podcast – like everyone in the 2020 year with COVID we started a Podcast, it was based on interviewing a leader to understand what made them tick and their leadership journey. It was a great podcast, we did 52 in 52 weeks and then we stopped but we loved the interviews and we got some regular listeners.

• Listings – consulting listings, female network listings and other listings to ensure that we would come up if people were looking

• Website – constant updates to website to ensure new and interesting information

• Brochures – regular brochures that are hard copy and soft copy about our service

• Email campaigns – through Linkedin and/or through Mailchimp through regular newsletters.

• And other things that I now consider marketing…..

It’s hard to measure the success of the marketing stuff listed about but then you speak with a potential client, bump into someone that wants to partner on something or someone reaches out on Linkedin off the back of your postings or seeing some new content.

But whatever the case brand and marketing is important. It’s sometimes hard to measure, but there is ROI. You just need to find the right balance between spend and ROI.

Companies these days, larger companies can measure ROI on marketing campaigns more successfully than they have been able to in the past, which helps them invest in retention, but the cost of acquisition is always a challenge, for most businesses.

When you own a consulting business, the marketing play is a long play, not a short play and therefore you need to be comfortable with what you invest and the return you will make in the short term, and the long term.

So, I am a frustrated marketer and like to see the difference that certain campaigns have on statistics at month end and understand how to make them improve month-on-month. Measuring the key engagement stats every month also helps to understand what people that are engaging with the business enjoy.

If you are looking for a marketing expert, you’ve come to the wrong place LOL, however if you are looking for a frustrated marketer that has learnt to love marketing and all things associated with it, as I founder my business, you’ve come to the right place.

We have some cool content and always something new prepared to read, new templates, new industry reports or we always have something to say, so tune in and you’ll see our content strategy in real time.

I hope you like this article, I had fun writing it. 🌞

You might want to explore other thought leadership articles

How should we think about Complexity? Is it complicated?

Mark Easdown writes about complexity. In the mid 1980s, a school of thought emerged around “Complexity” and “Complex Adaptive Systems” with the formation of the Sante Fe Institute, formed in part by former members of Los Alamos National Laboratory. The institute drew from multi-disciplinary domains and insights of : economics, neural networks, physics, artificial intelligence, chaos theory, cybernetics, biology, ecology and archaeology. Theories on Complexity and Complex Adaptive systems sought to develop common frameworks and understandings of physical and social systems that was an alternate to more linear and reductionist modes of thinking.

Article written by Mark Easdown

Business Planning, Mental Models, Ways of Thinking & Working

“A complicated system is the sum of its parts. You can solve problems by breaking things down and solving them separately. In a complex system, the properties of the whole are the result of interaction between the parts and the linkages and the constraints. In fact, in a complex system how things connect is more important than what they are. So, the properties of that emergent pattern can never be decomposed to the original parts.” David Snowden

“The problem is complexity (in financial markets) …we cannot prepare for every thread of causality through every interaction; in the speed of the event we find there is no time to make adjustments.” Richard Bookstaber

“Nature likes to over-insure itself. Layers of redundancy are the central risk management property of natural systems.” Nassim Taleb

In the mid 1980s, a school of thought emerged around “Complexity” and “Complex Adaptive Systems” with the formation of the Sante Fe Institute, formed in part by former members of Los Alamos National Laboratory. The institute drew from multi-disciplinary domains and insights of : economics, neural networks, physics, artificial intelligence, chaos theory, cybernetics, biology, ecology and archaeology. Theories on Complexity and Complex Adaptive systems sought to develop common frameworks and understandings of physical and social systems that was an alternate to more linear and reductionist modes of thinking. Members sought to better understand spontaneous, self-organising dynamics and found examples in the;

Natural World - Brains, Immune Systems, Ecologies, Cells, Developing Embryos and Ant colonies

Human World – Political parties, Scientific communities and in the economy

Why bother?

Just say you and your team are facing a complicated problem, then you may break down the problem into component parts, build an expert team internally or partner with external consultants, you may take a data driven or fact-based approach, you may identify best practices create a strategic plan and solve the problem incrementally. However, is that all? Is there a one size fits all solution to problem solving?

What if your problem could be categorised with traits such as;

Levels of uncertainty, ambiguity, unpredictability, dynamic interfaces - many diverse and independent parts that were interrelated, interdependent and linked through many interconnections into a network

The properties of the whole cannot be predicted from the behaviours of the component parts, in fact the network of many components may be gathering information learning and acting in parallel in an environment produced by these interactions – the system co-evolves within its environment

There may be significant political, social or external influences

“Wise executives tailor their approach to fit the complexity of the circumstances they face.” David Snowden & Mary Boone

Where in the real world might it be useful to have sound thinking about complexity and solving problems?

In Project Management

Programs of work and problems to solve come in a variety of forms, at the simpler end of spectrum process re-engineering and best practices serve us well to achieve desired outcomes. Yet increasingly, our problems to solve are complicated, we need to analyse things to figure out what to do and cause and effect are distanced. Complex projects are harder still, they display behaviours such as self-organising, emergent properties, non-linear and phase transition behaviours. We need a different mindset, structure and strategy to wrestle with these problems.

In Financial Markets

These are complex adaptive systems, tightly coupled with unexpected feedback loops, with investors of different investment styles & horizons, the sum of the parts will not explain the whole in a linear manner, there are infrequent extreme price moves, not normally distributed.

In Nature

Complex collective behaviours are displayed when individual ants forage for food and lay down a pheromone trail on the way out from the colony and if successful finding food lay down even more on way back to the colony. Other ants follow this stronger pheromone trail to the food adding their pheromone. So, the pheromone trail becomes the whole colonies best path to food, it is an ant colony optimisation algorithm. Interestingly, this insight has helped form the basis of swarm intelligence and a wide array of solutions across routing and scheduling problems and bayesian networks.

The twenty-first century will be the "century of complexity" Stephen Hawking

COMPLEX PROGRAMS

“Strategy in complex systems must resemble strategy in board games. You develop a small and useful tree of options that is continuously revised based on the arrangement of the pieces and the actions of the opponent. It is critical to keep the number of options open. It is important to develop a theory of what kinds of options you want to have open” - John H Holland

In complex situations "cause and effect are only coherent in retrospect and do not repeat" - Sarah Sheard

Complex problems to solve are unique and they challenge some of the traditional approaches to program and risk management thinking, which may emphasise a need to identify risks in order to control them or completely plan and control programs of work. Examples of complex programs may include: computer systems and networks, buildings, bridges, planes, ships and automobiles.

Let’s take a look at what makes complex programs unique;

Sophisticated structures with many component parts interacting with each other, giving a degree of uncertainty whereby you may not know what you don’t know until it occurs

Unknowable interdependencies across domains, a need for agility and structures that favour the decentralised and local to the centralised approach.

There may be interfaces with complementary projects which present challenges in scheduling of these interconnected systems, teams and resources

The environment may have a political realm where new government decisions or public policy arises

So, what is a desirable mindset for complex programs?

A Forward focus, a willingness to proactively manage project development and critical issues through agility, collaboration and adaptability. You may need nuanced responses and local innovation.

Analysis of likely origins of complexity and thinking through dependencies, seek critical junctions, vulnerabilities & countermeasures. Contingency planning around time, buffering on sequencing, budget and people skills

Dynamic reporting and monitoring, a willingness to pick up early warning signs and take corrective actions

Communications will be dynamic, real time & high visibility (as small changes can have oversized consequences amplified by scale of some projects)

Program planning may have both a single view and multiple integrated project schedules

Cynefin is a framework to deal with predictable and unpredictable worlds (David Snowden)

In 1999, David Snowden described a framework and problem-solving tool which helps to adjust management style to fit circumstances, and has relevance across product development, marketing, organisational design and BCP/DR and crisis management. The framework had 5 domains;

OBVIOUS. Options are clear, steps to success are known, variables well known, cause-effect relationships are apparent, you are able to assess the situation, follow a procedure, categorise its type and base your response on best practice (processes & procedures) and feasible to achieve best possible result. Examples: Product mass production, cooking with a recipe, known scientific issues, known legal issues.

COMPLICATED. Solutions not obvious to everyone but most variables involved are well known, cause-effect relationships are apparent, you may assess a situation, build a diverse team or utilise experts to deliver the best response. The best that can be achieved is a good result, maybe not the best result. Examples: Existing product enhancements, coaching a team, adopting new approaches, hiring process.

COMPLEX. The context is often unpredictable, many factors uncertain, many variables may intervene, data may be incomplete, it may not be possible to determine right options, make predictions or find cause-effect relationships, there may be multiple methods to address issues. Exploring what has a proven record in past situations, small tests or business experiments, simple guidelines, brainstorming, innovation and creativity may drive solutions. Examples: weather predictions, stock markets, poker, epidemic controls.

CHAOTIC. The situation is where nobody knows what to expect, anything can happen, it is impossible to make predictions. You may have to act towards the urgent and important, then check and evaluate result before responding to that result and acting again. Examples: Innovate new products, anything which predicts people’s preferences or behaviours, crisis event and crisis management, warfare

DISORDER. The situation is not known, you need to firstly move to a known domain & gather more information.

COMPLEXITY IN FINANCIAL MARKETS

“In the last few years the concept of self-organising systems – of complex systems in which randomness and chaos seem spontaneously to evolve into unexpected order – has become an increasingly influential idea that links together researchers in many fields, from artificial intelligence to chemistry, from evolution to geology. For whatever reason, however, this movement has so far largely passed economic theory by. It is time to see how the new ideas can usefully be applied to that immensely complex, but indisputably self-organising system we call the economy” - Paul Krugman 1996

“By one estimate, 90% of international transactions were accounted for by trade before 1970, and only 10% by capital flows. Today, despite a vast increase in global trade, that ratio has been reversed, with 90% of transactions accounted for by financial flows not directly related to trade in goods and services.” - Didier Sornette 2003

“Fundamental analysis seeks to establish how underlying values are reflected in stock prices, whereas the theory of reflexivity shows how stock prices can influence underlying values. One provides a static picture, the other a dynamic one.” - George Soros

Financial markets have all the basic components of complex adaptive systems, namely:

Investors have differing investment strategies and horizons from trading at the speed of light to long term cyclical horizons. They take external information and combine it with their own strategic intent and these compete in financial markets => this is adaptive decision making

Financial markets is the aggregation of large-scale collective decision making and actions => these are developing, complex and emergent

Financial markets exist in a non-equilibrium state , are non linear, they experience non-frequent extreme price moves with the aggregate behaviour more complex than would be predicted by the sum of the individual parts.

Financial Markets are subject to feedback loops, where the result of one iteration becomes an input of next iteration

So, how has the emerging knowledge of complexity and financial markets framed regulators thinking?

The global financial crisis highlighted the complexity, leverage, inter-connected and tightly coupled of financial markets. In response we have seen;

Efforts to reduce interconnectedness (intra-day local trading halts, regional collateral exchanges)

Enhanced capital rules (increased contingency buffers and incentives for some activities to be managed by non-bank sector & efforts to reduce concentration of risks)

Enhanced liquidity rules (increase quantum and quality of contingency buffers)

Speed, agility and quantum of central bank and treasury initiatives to address market panics and crisis

A re-think of the rule-making complexity and mental models applied to finance;

“Modern finance is complex, perhaps too complex. Regulation of modern finance is complex, almost certainly too complex. That configuration spells trouble. As you do not fight fire with fire, you do not fight complexity with complexity. Because complexity generates uncertainty, not risk, it requires a regulatory response grounded in simplicity, not complexity. Delivering that would require an about-turn from the regulatory community from the path followed for the better part of the past 50 years. If a once-in-a-lifetime crisis is not able to deliver that change, it is not clear what will.” - Andrew Haldane Bank of England Speech 2012 “ The Dog and the Frisbee” [https://www.bis.org/review/r120905a.pdf ]

COMPLEXITY IN NATURE

In her TED Talk, Deborah Gordon: The emergent genius of ant colonies: highlights an example of a complex adapative system with no central control or management in an ant colony: [ https://www.youtube.com/watch?v=ukS4UjCauUs]

So, what is the strategy of the ant colony to constantly adapt to its complex environment? As per Deborah Gordon studies;

The ant colony allocates simple roles

At any given time 25% are patrolling, foraging and doing maintenance, 25% are inside with queen ant doing maintenance and looking after larvae, and finally 50% appear to be contingency and in reserve, able to surge as required to collect more food, patrol or more maintenance.

Communications are not centralised, they are dynamic, simple and local rules to adapt to emergent environment

The process is noisy, messy, imperfect and requires individual dynamic communications

Ant colonies can learn at the individual level by trial and error over many generations but this can nurture collective memory and problem-solving skills. The local instructing the central.

“So, the key to unlocking the efficiency of a leaderless system will rely on, among other things: clear role definition, flexible task allocation, a sense of responsibility toward the group, and shared understanding and response to communication patterns. Organizations would need to make an incredible investment in their employees, and vice versa.” Amanda Silver – Organising complexity – How Ant colonies self-manage. [https://medium.com/swlh/organizing-complexity-how-ant-colonies-self-manage-50455358f3cd]

How we should think about complex domains is still evolving, a multi-disciplinary lens across research and practice has been adding to this knowledge pool for decades. It is a vital enquiry for humankind, especially as our challenges become more complex to solve and our climate is as a complex adaptive system.

‘“he climate is a common good, belonging to all and meant for all. At the global level, it is a complex system linked to many of the essential conditions for human life.”- Pope Francis 2015

LOOKING TO CURATE YOUR BUSINESS STRATEGY? REACH OUT.

Whiteark is not your average consulting firm, we have first-hand experience in delivering transformation programs for private equity and other organisations with a focus on people just as much as financial outcomes.

We understand that execution is the hardest part, and so we roll our sleeves up and work with you to ensure we can deliver the required outcomes for the business. Our co-founders have a combined experience of over 50 years’ working as Executives in organisations delivering outcomes for shareholders. Reach out for a no obligation conversation on how we can help you. Contact us on whiteark@whiteark.com.au

Article written by Mark Easdown

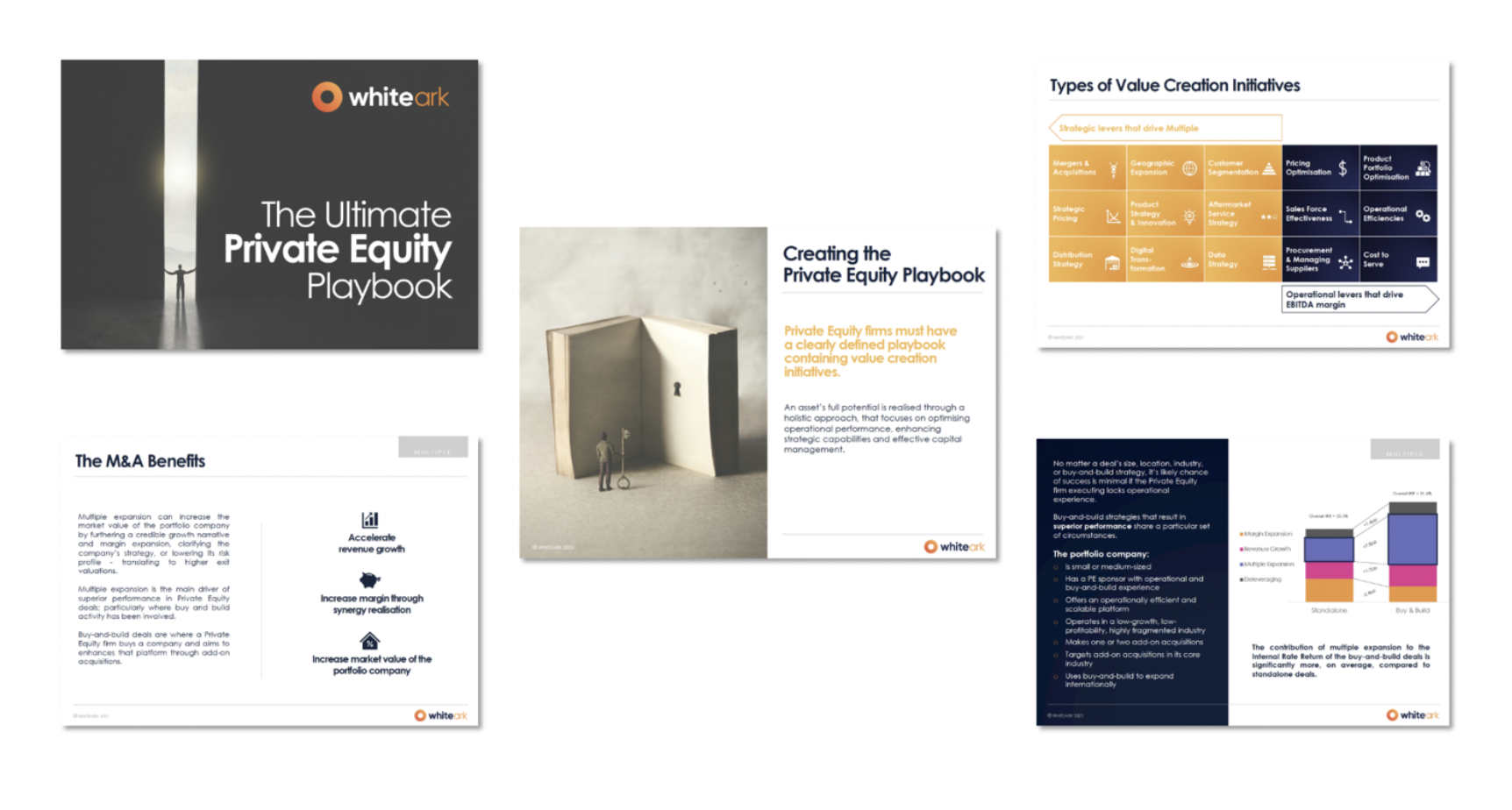

Driving value creation

Jo Hands writes all about driving value creation. Value creation is a word that’s used a lot, but what does it mean? Creating value - customer, consumer and financial. When a company buys a business, they focus on value creation. The business case assumes that there is value to create. This value can be created by pulling either strategic or operational levers.

Value creation is a word that’s used a lot, but what does it mean? Creating value - customer, consumer and financial. When a company buys a business, they focus on value creation. The business case assumes that there is value to create.

Value can be created by pulling either strategic or operational levers:

Mergers and Acquisitions: Buy-and-build deals are where a Private Equity firm buys a company and aims to enhances that platform through add-on acquisitions.

Strategic Pricing: Strategic pricing incorporates best pricing practices and ensures that your pricing strategies, analytics and processes complement your business strategy. A product’s price is based on the value to the customer, or on competitive strategy, rather than on the cost of production. By creating strategic pricing policies, analytics, and processes, you can directly capture customer value and translate to shareholder value.

Distribution Strategy: Distribution strategy is a plan to make a product or a service available to the target customers through its supply chain - to make sure the it can reach the maximum potential customers at minimal or optimal distribution costs. A good distribution strategy can maximise your revenue and profits.

Geographic Expansion: With access to new markets, a business has the potential to build a new customer base.

Product Strategy: A product strategy outlines the desired outcomes to be achieved by the product including the end-to-end vision, and how it supports the company’s strategic objectives. The product strategy is brought to life through the product road map and can be used to support any tactical decisions that the company needs to make.

Product Innovation: Product innovation represents a new way of solving a problem a high number of consumers have:

There are no products on the market that address the problem statement - unexplored market spaces could potentially generate high profits or;

There may be other products on the market that address the problem but in a different way to your innovative solution

Digital Transformation: Digital transformation is the use of technology — software enabled, connected, transactions, and interactions, across all areas of a business. The goal of digital transformation is disrupting existing business models, improving customer experience, and creating operational efficiency to drive economic value creation.

Customer Segmentation: the benefits of customer segmentation include focus, competitiveness, expansion, retention, communications effectiveness and profitability.

Aftermarket Service Strategy: The concept of aftermarket service is as important as sales, the saying “it takes years to build a reputation but just moments to ruin it” addresses the importance of keeping a customer happy and satisfied. Aftermarket service does not generate any revenue for the company, but it increases the goodwill in the market and amongst the customers.

Data Strategy: Data strategy is a central, integrated concept that articulates how data will enable and inspire business strategy.

Pricing Optimisation: Price optimisation is the practice of using data from customers and the market to find the most effective price point for a product or service that maximizes value for customers and sales or profit for the company.

Sales Force Effectiveness: Sales force effectiveness is driven by the decisions, processes, systems and programmes that sales leaders are accountable. By managing sales force effectiveness drivers, companies can build high-quality sales teams that better meet customer needs, increase productivity and successful conversion, and consequently result in improved turnover and EBITDA margins.

Procurement & Managing Suppliers: Smart procurement practices are fundamental for companies across all industries to optimise operational efficiencies and improving EBITDA margin.

Product Portfolio Optimisation: Product portfolio optimisation helps managers assess their products’ current level of success - it provides a centralized view of an entire suite of products against the prevailing marketplace for those products. Effective product portfolio optimisation highlights future opportunities for improved resource allocation, greater returns, growth and profit, and reveals products that are generating a negative contribution.

Operational Efficiencies: Operational efficiency refers to a company’s ability to reduce waste in time, effort and materials as much as possible, while still producing a high-quality service or product. Financially, operational efficiency is the ratio between the input required to keep the company going and the output it provides. When improving operational efficiency, the output to input ratio improves. The greater the operational efficiency, the more profitable a company becomes as it can generate greater income or returns for the same or lower cost.

Cost to Serve: Cost to Serve focuses on aggregate analyses around a blend of cost drivers. The analysis exposes the variation in customer demands for different activities and has a different cost profile. Without understanding the cost to serve a customer, a company is unable to determine the value that customer is contributing to their business.

The value levers are a great way of prioritising what's important.

The levers that drive the biggest value result in an improved performance that leads to greater valuation.

If you are:

1. Getting your business ready for sale

Executing initiatives that drive value and can be in the run rate results will result in a higher sale price

2. Buying a business.

Your investment case is critical to drive the appropriate acquisition price. This will also drive what transformation program looks like once the business has been bought to ensure the business case is achieved/exceeded

3. Running your own business.

Driving value is what you do everyday but sometimes it's easy to miss the levers to pull to achieve the greatest success.

At any point of a business lifecycle it's imperative that driving value is something you focus on to drive consistent and stable earnings with a positive trend.

Article by Jo Hands, Co-Founder Whiteark

Looking for more support? Download our Private Equity Playbook for the ultimate guide to value creation.

Looking to create value in your organisation? Let us help.

Whiteark is not your average consulting firm, we have first-hand experience in delivering transformation programs for private equity and other organisations with a focus on people just as much as financial outcomes. We understand that execution is the hardest part, and so we roll our sleeves up and work with you to ensure we can deliver the required outcomes for the business.

Our co-founders have a combined experience of over 50 years’ working as Executives in organisations delivering outcomes for shareholders. Reach out for a no obligation conversation on how we can help you. Contact us on whiteark@whiteark.com.au

The Problem Is …. How to Solve It?

Mark Easdown writes about problem solving… Good problem solving needs: cognitive diversity, valuing dissent to mitigate consensus “fails” & “group think”, a clear approach in stressful situations, switch thinking or adding some randomness to process, a healthy power relationship (no hubris or silencing of opposition, a need for participative management & subordinate assertiveness training), multiple approaches to problem solving …

Article written by Mark Easdown

Individuals, Teams & Enterprise, Mental Models, Ways of Working

““A problem well put is half solved.””

““I think that there is only one way to science – or to philosophy, for that matter: to meet a problem, to see its beauty and fall in love with it; to get married to it and to live happily, till death do ye part – unless you should meet another and even more fascinating problem or unless, indeed, you should obtain a solution. But even if you do obtain a solution, you may discover, to your delight, the existence of a whole family of enchanting, though perhaps difficult, problem children …””

““By operating without a leader the scout bees of a swarm neatly avoid one of the greatest threats to good decision making by groups: a domineering leader. Such an individual reduces a group’s collective power to uncover a diverse set of possible solutions to a problem, to critically appraise these possibilities, and to winnow out all but the best one.””

““Probably he played it the way he did because it was not a good piano. Because he could not fall in love with it he found another way to get the most out of it.” ”

Did you know ?

3M has a “flexible attention” policy (take a walk, nap, play a game) as they know creative ideas and problem solutions can sneak up on us as we pay attention to something else. Ideas flow between silos with engineers rotated between departments each few years.

Problem solving is a process followed to find solutions to difficult or complex issues.

What might that look like ?

Variances & deviations from desired outcomes – this may be pleasant (an opportunity) or unpleasant (Apollo 13)

For a problem to be solved suggests some precision in description, identification, root cause

Maybe we have a criterion that our best explanation or lived experience just fails to meet

An exploration of problem solving uncovers useful practices, shines a light on power structures and reveals a wider array of human perceptions, traits & group dynamics;

Author Charlan Nemeth in “No! , The power of disagreement in a world that wants to get along” highlights the case of United Airlines Flight 173, in the days before Christmas in 1978 flying from NY to Portland Oregon, USA. As the plane approached Portland it lowered the landing gear and the cockpit heard a large thump with the plane vibrating and rotating. The pilot questioned the landing gear, aborted landing and put the plane into a holding pattern. For 45 minutes, pilot and crew investigated the flight panel & landing gear problem yet overlooked the fact the plane proceeded to run out of fuel, falling out of sky, killing 10 people of the 196 on board, just six miles from airport. How can this problem solving go so tragically wrong?

Good problem solving needs: cognitive diversity, valuing dissent to mitigate consensus “fails” & “group think”, a clear approach in stressful situations, switch thinking or adding some randomness to process, a healthy power relationship (no hubris or silencing of opposition, a need for participative management & subordinate assertiveness training), multiple approaches to problem solving (broad information search, multiple alternatives considered), a human tendency to not see a solution if it is at odds with majority judgement, the very action of voicing dissent with conviction will alter the perception & awareness of others.

Maybe the way things “are” differ from our best thinking or theory on the way things “should be” .

Let’s take a look at Problem Solving & Mental Models across a few domains; In Adversity, In Manufacturing, In Investment Markets and In Nature

Producing your finest problem solving & improvisation, driven on by adversity

“”Messy : How to be creative and resilient in a tidy-minded world””

In January 1975, 17 year old Vera Brandes stood on the stage of the Cologne Opera House, awaiting a full house, as the youngest concert promoter in Germany. Vera had convinced American Jazz Pianist, Keith Jarrett to perform a solo recital, had arranged the grand concert hall, invited 1,400 people and arranged for delivery of a very specific & artist requested Bosendorfer 290 Imperial concert grand piano.

The problem for Vera’s project was that the opera house staff had wheeled out the wrong piano and gone home. They had wheeled out a small piano which would not produce enough sound to reach the furthest balconies, the piano was out of tune, the black notes in the middle of the keyboard didn’t work, the piano pedals were stuck – it was unplayable. In the scarce time before the concert, the local piano tuner concluded that given the heavy rain outside, a substitute piano would not survive the transitional trip from nearby storage facility.

Technicians spent several hours trying to make the piano sound halfway decent, the high and low notes jangled, the piano pedals malfunctioned and even the performer was suffering from several days of back pain and wearing extra spinal support. Understandably Keith Jarrett refused to play, but Vera Brandes cajoled, pacified & pleaded and at 11-30pm the concert finally began.

So with Vera Brandes project flashing bright red, what problem solving skills did Keith Jarrett deploy to overcome sub-optimal & malfunctioning tools ?

As the author says “ The minute he played the first note, everybody knew this was magic”, “It was beautiful and strange”, “ The Koln concert album has sold 3.5 million copies, no other solo jazz album nor piano solo has matched it”, “Jarrett really had to play the piano very hard to get enough volume to the balconies”, “ ….”handed a mess, Keith Jarrett embraced it, and soared”.

Toyota Business Practices (TBP) – A problem solving model

Toyota has a rich and deep history of instruction, values, actions shared, practiced, experienced and refined by many staff across many cultures around the world. Its Best Practices are constantly evolving. Toyota Business Practices are an example of tangible approaches to daily work, the essence of TBP is a problem solving model. Whilst a mastery is achieved across time and through daily work and with a mindset of drive and dedication, a basic summary includes the following elements;

Toyota defines “a problem” as a gap between the current state (as is) and future/ideal state (to be). The concept of problem is not viewed as a negative, as to find problems and to take countermeasures to eliminate them leads to continuous improvement.

““No one has more trouble than the person who claims to have no trouble””

A summary of the basic steps of Toyota Problem Solving, 2006 includes;

1. Clarify the Problem: requires understanding and pre-emptive thinking around: Ultimate Goal (what is the contribution, the purpose, how is it realised and for whom?), Current Situation ( talk to people involved, observe, concrete terms) & Ideal Situation ( a clear standard result to be achieved after problem is solved, it is a concrete & achievable and contributes to the ultimate goal)

2. Break down the Problem: requires qualitative and quantitative analysis, prioritise and break down bigger problem into smaller and more concrete ones to observe and find the point of occurrence

3. Set a Target: A target is measurable & states by when & is challenging in nature

4. Analyse the Root Cause: look at the point of occurrence & cascade thinking through asking why & seek peer review. If the countermeasures are applied to something other than root cause – this leads to wasted effort and resources

5. Develop countermeasures: develop many versions, select highest value-add & compliance, build consensus , make clear action plans

6. See countermeasures through: implement with concerted efforts, speed & persistence, share information, inform, report and consult, trial and error to expected results

7. Monitor results & process: ensure targets achieved, understand reasons for success or failure and accumulate continuous improvement knowledge

8. Standardise Successful Process: establish new standard and start next round of continuous problem solving / PDCA

““I have found it helpful to think of my life as if it were a game in which each problem I face is a puzzle I need to solve. By solving the puzzle, I get a gem in the form of a principle that helps me avoid the same sort of problem in the future. Collecting these gems continually improves my decision making, so I am able to ascend to higher and higher levels of play in which the game gets harder and the stakes become ever greater.” ”

Ray Dalio – Principles & Problem Solving in Investment Management

In 1975, Ray Dalio founded Bridgewater Associates which went on to become the world’s largest hedge fund by 2005. He is known as a successful investor, innovator and aimed to structure global portfolios with uncorrelated investment returns, with allocations based on risk analysis rather than by asset classes. In 2011, Ray & Barbara Dalio established a philanthropic foundation and pledged to donate more than half their fortune in their lifetimes. In 2011, he self-published on-line his philosophy of investment which evolved to be an acclaimed 2017 book “Principles” on corporate management and investment. An overview of the framework Ray Dalio approaches problem solving includes;

1. Have Clear Goals: You cannot have everything – prioritise, don’t conflate your goals with just desires and decide what you really want, setbacks are important to making progress – in bad times you may need to modify goals to preserve what you have.

2. Identify & don’t tolerate problems: a useful mind hack if that painful problems are usually a good signpost you have a problem worth diagnosing and improving, don’t avoid problems as they are rooted in harsh and unpleasant realities, be precise and specific with your problem description, pull apart causes and the real problem, fix problems that yield biggest returns and take care small problems are not symptoms of larger ones, failing to address a problem has the same consequences as failing to identify it.

3. Diagnose problems to get at their root causes: don’t jump immediately into solution mode, identify “what” before commencing “what to do about it”, you must identify the root cause – not proximate ones, sometimes you will find the root cause is people or system or process, it can be a painful journey to resolution

4. Design a Plan: visual what you need to do to achieve goals, what needs to change to produce better outcomes, there are possibly many pathways – you just need to find one that works, create a narrative and time lines, identify tasks that connect to the narrative to achieve goals.

5. Push through to completion : you will need self-discipline, good work habits (well organised, to-do lists, priorities) are vastly underrated, establish clear metrics, have another monitor your results, as you discover new problems – repeat

Dalio’s problem solving mental models also covers: self-awareness (knowing your weakness & staring into them is a first step to success), seek to understand what your missing, be humble & radically open-minded (address ego and blind spot barriers), beware of harmful emotions, first learn then decide, simplify, use principles, determine who you should be listening to and what is true, be very specific about problems – don’t start with generalisations, convert your principles into algorithms and have these make decisions alongside you.

“The Waggle Dance” – Nest site selection & group decision making

In the 1950s, Martin Lindauer published a study on house hunting by honey bees and observed that bee scouts perform “waggle dances” on the surface of a swarm to advertise potential new nest sites. Advancing this research Cornell biologist Thomas Seeley noted the process was “complicated enough to rival the dealings of any department committee”, as potentially 10,000+ bees will relocate and need an efficient process to narrow alternatives and mitigate risks of bad decisions. When a hive gets too crowded, its queen and half the hive will swarm to a nearby tree and wait for several hundred scouts to go house hunting. Seeley notes “the bee’s method, which is a product of disagreement and contest rather than consensus and compromise, consistently yields excellent collective decisions”

Let’s explore the bee’s problem to solve;

The bee colony survival is as stake, so an accurate decision is required. New home must be suitable for rearing brood and storing honey and offer protections from: predators, thieves and bad weather.

A speedy decision is required, as the more hours the entire hive is exposed to elements it loses energy and reserves

A unified choice is required. Communications and contestability are crucial, a split decision could be fatal

What can bees teach us about problem solving & decision making?

Whilst the problem to solve is of a clear and stable nature, information may be incomplete or inaccurate

Information in a complex environment may be constantly evolving and changing

Bees use hundreds of independent, widely distributed scouts who return with heterogeneous information (differing constituents, dissimilar components, non-uniform in composition) which may be better or worse and is shared with other scouts by way of a waggle dance, no scout is stifled & the swarm leverages its collective intelligence.

So, how do they find consensus as any individual scout has only direct experience with select potential sites, yet many are examined and considered?

It is in the friendly competition between scouts and the various coalitions all vying for favoured sites, the exercise is not solved with “group-think”, rather a scout may leave the swarm cluster and go to examine potential site to judge its merit. There is no need for an individual scout to have a macro global view of all alternatives, nor a need to tally and compare votes – it is the smarts of the swarm working as individuals or collectives making speedy, accurate and unified assessments.

To recap

As we have seen across multiple domains and across several mental models, problems are not necessarily a bad thing – sometimes they are a pathway to travel to deliver quality strategic outcomes, sometimes they are a link in a chain of continuous improvement (kaizen), if they are material they must be addressed to mitigate severe consequences (Flight 173, Investment Returns and bee hive nest selection), a structure and process is very useful, to solve problems will often reveal some uncomfortable truths about the nature of the individuals, the group, power structures, communications and these must also be confronted and resolved.

Yet, as Keith Jarrett demonstrated bringing passion, intelligence, skill, pragmatism and persistence to problem solving, can yield your teams greatest moment. White Ark is here to help you.

When Richard Feynman faces a problem, he's unusually good at going back to being like a child, ignoring what everyone else thinks... He was so unstuck --- if something didn't work, he'd look at it another way." --- Marvin Minsky, MIT

LOOKING TO CURATE YOUR BUSINESS STRATEGY? REACH OUT.

Whiteark is not your average consulting firm, we have first-hand experience in delivering transformation programs for private equity and other organisations with a focus on people just as much as financial outcomes.

We understand that execution is the hardest part, and so we roll our sleeves up and work with you to ensure we can deliver the required outcomes for the business. Our co-founders have a combined experience of over 50 years’ working as Executives in organisations delivering outcomes for shareholders. Reach out for a no obligation conversation on how we can help you. Contact us on whiteark@whiteark.com.au

Article written by Mark Easdown

Transforming your Sales and Service Model

Are you ready to take on a bold sales and service model transformation? Now is the time to reinvent your model and integrate the value your business provides into the “new” societal landscape post the global disruption of Covid-19. In today’s environment, your successful sales and service transformation will be enabled by strong leadership, facts driven from data and analytical insights, and new approaches to technology.

Are you ready to take on a bold sales and service model transformation? Now is the time to reinvent your model and integrate the value your business provides into the “new” societal landscape post the global disruption of Covid-19. In today’s environment, your successful sales and service transformation will be enabled by strong leadership, facts driven from data and analytical insights, and new approaches to technology.

It is important that you remain flexible and resilient while looking to the future - redefine your operations so that you can emerge stronger than your competitors. You must pivot your sales and service models in response to the new societal landscape - purchasing power is shifting fast, the demand for digital channels is rising. To retain customers, protect revenues and realign go-to-market investments you must pivot your sales and service model to meet the constantly changing expectations of your customers.

Hold tight and embrace the uncertainty – be courageous and apply a different approach to how you would usually gain market share all while monitoring the shift in consumer demands to ensure you are ahead of the competition.

Below are the key considerations for redesigning your sales and service model:

Rediscover your customer - understand your customers so that you can meet their evolving wants and needs so that you can remain relevant

Redefine the sales and service journey – segment your customers and focus your efforts on the strongest and most profitable opportunities

Enhance your product/service offering to meet customer expectations - reinvent through new narratives, approaches and terms, and diversify dynamic offers

Enable your team with the tools and skills to succeed in today’s digital age – ensure you provide your team with the key enablers that they need to support them in being successful including training and coaching, sales tools, technology

Reward your sales and service resources for the right behaviour/outcomes – align on priorities, determine the metrics to monitor, measure performance and reward success to keep your workforce motivated

If you need help with transforming your sales and service model to meet the needs of customers in today’s environment, please reach out to Whiteark for a no obligation consultation and we can help you navigate your future to success.

Forecasting

Mark Easdown writes about forecasting. The prediction process starts with propositions, then verified, quantified and made actionable. A robust peer review occurs and 95% of predictions are modified along the way. Plummer routinely scrutinises predictions with actual events and these results are highlighted at conferences – championing the successes and sharing insights across those that were wrong. “Nobody here is hired because they’re psychic; there hired to generate insights that are useful – even if they turn out wrong. It’s useful to get you thinking”.

Article written by Mark Easdown

Decision Making & Planning, Ways of Working with Uncertainty

“The only function of economic forecasting is to make astrology look respectable.”

“Forecasts usually tell us more of the forecaster than of the future.”

“There is great value in bringing together people who attempt to address a common problem of forecasting from different perspectives and based on very different kinds of data.”

“Your assumptions are your windows on the world. Scrub them off every once in a while, or the light won’t come in.”

“For superforecasters, beliefs are hypotheses to be tested, not treasures to be guarded.”

“I prefer true but imperfect knowledge, even if it leaves much indetermined and unpredictable, to a pretence of exact knowledge that is likely to be false.”

“The Lucretius underestimation, after the Latin poetic philosopher who wrote that the fool believes that the tallest mountain there is, should be equal to the tallest one he has observed.”

A forecast is a statement about the future. (Clements & Henry, 1998)

As authors of “Forecasting” (J.Castle, M.Clements, D.Henry) note; a forecast can take many forms;

Some are vague and some are precise, Some are concerned with near term and some the distant future

“Fore” denotes in advance whilst “Cast” might sound a bit chancy (cast a fishing net, cast a spell) or might sound more solid (bronze statues are also cast)

Chance is central to forecasting & forecasts can and often do differ from outcomes

Forecasts should be accompanied by some level of certainty/uncertainty, time horizon, upper/lower bounds

The domain in which the forecast occurs matter, especially if no-one knows the complete set of possibilities

The authors consider the history of forecasting;

Forecasting likely pre-dates recorded writing with hunter-gatherers seeking where game of predators might be, edible plants and water supplies. Babylonians tracked the night sky presumably for planting and harvesting crops

Sir William Petty perhaps introduced early statistical forecasting in 17th Century and thought he observed a seven year “business cycle”

Weather forecasting evolved with Robert Fitzroy in 1859, who sought to devise a storm warning system to enable safe passage of ships and avoid loss of vessels &/or ships staying in port unnecessarily. Forecasting of nature extended to hurricanes, tropical cyclones, tornadoes, tsunamis and volcanic eruptions.

Yet, history is littered with failures in forecasting, large and small;

Ambiguous forecasts from Oracles of Delphi and Nostradamus

UK storms 1987, with lives lost and approximately 15million trees blown down

Failure to predict 1929 Great Depression or severity of Global Financial Crisis, mid-2007 to early 2009

“When the Paris exhibition closes, the electric light will close with it and no more be heard of it” – Sir Erasmus Wilson & “a rocket will never be able to leave the earth’s atmosphere” – NY Times 1936

What do we want from forecasts ?

Do we want just accuracy? To what degree is that even possible across complicated and complex domains?

Do we want cognitively diverse teams to make us more aware of extreme events? Thus, minimising downside risks?

Do we just want comfort, ideological support and evidence of our existing beliefs? Do we want entertainment?

Do we want to influence a target audience, shift consensus or established beliefs?

These answers may differ if you are a CEO, CFO, Head of Sales, Head of Innovation, an Insurance Actuary, Epidemiologist, Politician, Economist, Intelligence Agency, Shock Jock or Sports Commentator.

For example, it was a mainstream view of epidemiologists across last 20 years that a pandemic was a prominent risk;

“The presence of a large reservoir of SARS-CoV-like viruses in horseshoe bats, together with the culture of eating exotic mammals in southern China, is a time bomb. The possibility of the re-emergence of SARS and other novel viruses from animals or laboratories and therefore the need for preparedness should not be ignored.”- David Epstein 2007

https://davidepstein.com/lets-get-ready-to-rumble-humanity-vs-infectious-disease/

https://cmr.asm.org/content/cmr/20/4/660.full.pdf

So, is COVID19 perhaps SARS2? Clearly, forecasting a pandemic is desirable. How do we give prominence to diverse voices & data and what are the better practices to observe and implement?

SUPER-FORECASTING

In October 2002, the US National Intelligence Estimates (a consensus view of the CIA, NSA, DIA and thirteen other agencies with > 20,000 intelligence analysts) concluded that the key claims of the Bush Administration claims about Weapons of Mass Destruction in Iraq were correct. After invading Iraq in 2003, the US found no evidence of WMDs. “It was one of the worst – arguably the worst - intelligence failure in modern history” notes Philip Tetlock and Dan Gardner in their book “Superforecasting : The Art and Science of Prediction”

In 2006, IARPA was formed to fund cutting-edge research with the aim of potentially enhancing the intelligence community work. IAPRA’s plan was to create a tournament-style incentive for top researchers (intelligence analysts, universities & a team of volunteers for the Good Judgement Project (GJP)), to generate accurate probability estimates to questions that were;

Neither so easy that an attentive reader of the NY Times could get them right , nor

So hard that no one on the planet could get them right

Approximately 500 questions spanned: economic, security, terrorism, energy, environmental, social and political realms

Forecast performance was monitored individually and in teams, and Tetlock’s GJP team proved 60% more accurate in year 1, 78% more accurate in Year 2.

What did these forecasting tournaments learn about the attributes of super-forecasters that may be of relevance in Commercial or Government organisations? Here are a few;

Superforecasters spoke in probabilities of how likely an event would occur (not in absolutes : yes/no), this better enabled them to accept a level of uncertainty – it made them more thoughtful and accurate

Superforecasters were often educated yet ordinary people with an open-mind, an ability to change their minds, humility and an ability to review assumptions & update forecasts frequently, albeit at times by small increments

Actions which were helpful included;

Breaking the question down into smaller components and identifying the known and the unknown, focus on work that is likely to have better payoff, actively seek to distinguish degrees of uncertainty, avoid binding rules. Consider the “outsiders” view, frame the problem not uniquely but as part of a wider phenomena

Examine what is unique about problem and look at your opinions and how they differ from other people’s viewpoints. Take in all the information with your “dragonfly eyes” and construct a unified vision, balancing arguments and counterarguments, balancing prudence and decisiveness – generating a description as clearly, concisely and as granular as possible

Don’t over-react to new information – a Bayesian approach was useful

The GJP found that while many forecasters were accurate within a horizon of 150 days, not even the super-forecasters were confident beyond 400 days, forecasts out to 5 years were about equal with chance.

What about forecasting teams versus forecasting individuals?

o With good group dynamics, flat and non-hierarchical structures and a culture of sharing – teams were better than individuals – aggregation was important. In fact teams of super-forecasters could beat established prediction markets.

o The note of caution around low performing teams came when people were lazy, let others do the work or where susceptible to group-think.

“Unchartered : How to map the future together.”

Daryl Plummer of Gartner, a technology advisory firm who produces forecasts for customers who wish to discern hype from reality.

The prediction process starts with propositions, then verified, quantified and made actionable. A robust peer review occurs and 95% of predictions are modified along the way. Plummer routinely scrutinises predictions with actual events and these results are highlighted at conferences – championing the successes and sharing insights across those that were wrong. “Nobody here is hired because they’re psychic; they’re hired to generate insights that are useful – even if they turn out wrong. It’s useful to get you thinking”.

The author notes “that what matters most isn’t the predictions themselves but how we respond to them, and whether we respond to them at all. The forecast that stupefies isn’t helpful, but the one that provokes fresh thinking can be. The point of predictions should not be to surrender to them but to use them to broaden and map your conceptual, imaginative horizons. Don’t fall for them – challenge them.”

“How to Decide” : Annie Duke – Simple Tools for making better choices

The author presents some useful tips that teams can use to elicit uninfected feedback and leverage the true wisdom of the crowd in decision making. This is especially useful where key forecast & value chain insights and institutional knowledge is held across multiple SMEs and stakeholders;

The Problem;

“When you tell someone what you think before hearing what they think, you can cause their opinion to bend towards yours, often times without them knowing it”, “The only way somebody can know that they’re disagreeing with you is if they know what you think first. Keeping that to yourself when you elicit feedback makes it more likely that what they say is actually what they believe”, “To get high quality feedback it’s important to put the other person as closely as possible into the same state of knowledge that you were in at the time you made the decision”, “Belief contagion is particularly problematic in groups”

Tips to elicit those insightful cross-functional perspectives;

Elicit initial opinions individually and independent before the group meets. Specify the type of feedback or insights required and request an email or written thoughts be provided before meeting. Collate these initial opinions and share with group prior to meeting. Now focus on areas of “diversion”, “dispersion”, avoid using any language around “disagreement”

Anonymise feedback to group – this removes any influence from the insights or opinions of higher status individuals

Anonymising feedback also gives equal weight to insights and opinion and allows outside-the box perspectives to be heard

Anonymised feedback will also allow mis-understandings to be discussed and the team to grow in knowledge together

If the team needs to make a decision within a meeting; try

Writing down insights and passing to one person to write on a whiteboard – maintaining anonymity

Writing down your insights and pass to another person to read aloud to the group

If you must read your own thoughts to group – start with most junior member and work towards most senior

“Radical Uncertainty: Decision Making for an unknowable future”

Authors: John Kay & Meryn King

“The belief that mathematical reasoning is more rigorous and precise than verbal reasoning, which is thought to be susceptible to vagueness and ambiguity, is pervasive in economics”& Jean-Claude Trichet of the 2007-2008 GFC; “As a policy-maker during the crisis, I found the available models of limited help. In fact, I would go further: in the face of the crisis, we felt abandoned by conventional tools”

The authors draw a number of helpful lessons in the use of economic and financial models in business and in government;

Use simple models and identify key factors that influence an assessment. Adding more and more elements to a model is to follow the mistaken belief that a model can describe the complexity of the real world. The better purpose for a model is to find “small world” problems which illuminate part of the large world radical uncertainty

Having identified model parameters that are likely to make a significant difference to your assessment, go and do some research in the real world to obtain evidence on the value of these parameters to customers or stakeholders. Simple models provide flexibility to explore the effects of modifications or scenarios.

A model is useful only if the person using it recognises it does not represent the world as it is really is, rather it is a tool for exploring ways in which decisions might or might not go wrong.

Uncertainty : Howard Marks : https://www.oaktreecapital.com/insights/howard-marks-memos/

In his May 2020 newsletter to Oaktree Clients, Howard Marks notes the field of economics is muddled and imprecise, there are no rules one can count on to consistently show causation, patterns tend to repeat, and while they may be historical, logical and often observed, they remain only tendencies. Excessive trust in forecasts is dangerous.

When considering current forecasts, he notes the world is more uncertain today than at any other time in our lifetimes, the ability to deal intelligently with uncertainty is one of the most important skills, the bigger the topic (world, economy. Markets, currencies, interest rates) the less possible it is to achieve superior knowledge and we should seek to understand the limitations of our foresights.

A forecast is a statement about the future, a future we cannot know everything about , yet it remains a useful tool for decision making, scenario modelling, stress testing and planning. The map is not the territory, so with forecasting we should learn from better practices around collating diverse views and data, building cognitively diverse teams, constantly challenging assumptions, leverage the wisdom & insights of your subject matter experts, maintain intellectual humility & resiliency facing uncertainty, use models wisely and adopt a bayesian approach.

“No amount of sophistication is going to allay the fact that all your knowledge is about the past and all your decisions are about the future.”

LOOKING TO CURATE YOUR BUSINESS STRATEGY? REACH OUT.

Whiteark is not your average consulting firm, we have first-hand experience in delivering transformation programs for private equity and other organisations with a focus on people just as much as financial outcomes.

We understand that execution is the hardest part, and so we roll our sleeves up and work with you to ensure we can deliver the required outcomes for the business. Our co-founders have a combined experience of over 50 years’ working as Executives in organisations delivering outcomes for shareholders. Reach out for a no obligation conversation on how we can help you. Contact us on whiteark@whiteark.com.au

Article written by Mark Easdown

How to deliver a successful transformation program

Jo Hands writes about how to deliver a successful transformation program. Nearly every project today is called a transformation. Most companies are changing, evolving and putting in programs to change the way things are done and these call these programs – ‘transformation project’s. It doesn’t matter what the programs are called, what matters is the that it achieves the outcome you are expecting.

Nearly every project today is called a transformation. Most companies are changing, evolving and putting in programs to change the way things are done and these call these programs – ‘transformation project’s. It doesn’t matter what the programs are called, what matters is the that it achieves the outcome you are expecting.

The statistics are terrible, however on average 20% of transformation programs achieve the required outcomes, this is a terrible statistic. Many companies put money, focus and effort into delivering the outcome however they are unable to deliver the required outcome.

Why?

There are four main reasons that transformation programs are not successful:

Success for the project has not been defined and is not well understood. Being very clear on what the project is trying to achieve, what is success and how the results are going to be measured is critical.

No Executive sponsorship – the Executive team do not sponsor the project and help show how important it is.

No accountability for the outcomes. The roles & responsibilities are not clear and the people running the program are not being held accountable and this flows down.

The organisation doesn’t want the change/they haven’t bought in and they make it so hard that the organisation gives up. It’s all too hard.

Once one or all of the 4 above happen the transformation program will likely not be successful, will not deliver the required outcome and next time people try they will say we tried this and it doesn’t work in our company.

No one sets out for it not be successful so how to do maximise the chance of success for your transformation program. There are four main things that will help maximise success:

Be very clear on what success is – define success, work out how to measure success & ensure you communicate this change to people impacted and key stakeholders

Ensure you have an Executive Sponsor that will support and drive the project and help clear blockages that are in the way

Build a change champion network in the organisation – key people that can champion change and support the program

Demonstrate progress and the ‘what is in it for me’ mentality to show people why change can be great

The success of transformation will be driven from the ability of the lead:

To set up the program for success

To get buy in

To not listen to naysayers

To focus on delivering outcomes and communicating

To build out the what is in it for me

The lead for the transformation needs to be very strong leaders, someone who is not worried or concerned about driving change and showing resilience.

From experience, I have seen many transformations go really well. I am someone who doesn’t like to give up and I like to be on the winning team – everyone makes mistakes and from these comes learnings and experience that helps you when you do your next program/project/transformation.

At Whiteark we love helping our clients with transformation; focused on ensuring that we can use our experience to help ensure their transformations are successful. If you are interested in having a conversation about how we can help you, reach out.

Need support in your transformation project? Reach out.

Whiteark is not your average consulting firm, we have first-hand experience in delivering transformation programs for private equity and other organisations with a focus on people just as much as financial outcomes.

We understand that execution is the hardest part, and so we roll our sleeves up and work with you to ensure we can deliver the required outcomes for the business. Our co-founders have a combined experience of over 50 years’ working as Executives in organisations delivering outcomes for shareholders. Reach out for a no obligation conversation on how we can help you. Contact us on whiteark@whiteark.com.au

Article by Jo Hands, Co-Founder Whiteark

Linking transformation to strategy

In today’s business environment, transformation can take many forms but no matter the type it revolves around the need to generate new value - unlock new opportunities, drive new growth, deliver new efficiencies. It is critical that the transformation project aligns to the company’s strategy – strategy is fundamental in guiding/aligning decisions and actions to ensure they support the achievement of the company’s strategic goals.

In today’s business environment, transformation can take many forms but no matter the type it revolves around the need to generate new value - unlock new opportunities, drive new growth, deliver new efficiencies.

It is critical that the transformation project aligns to the company’s strategy – strategy is fundamental in guiding/aligning decisions and actions to ensure they support the achievement of the company’s strategic goals. A sound strategy helps shape an executable transformation objective.

The value that your transformation project will create/deliver must be aligned to your company strategy and it will help with articulating desired transformation outcomes, from a financial perspective or from an operational perspective.

Once you have aligned your transformation ambition you can build out your transformation program.

THE STEPS

Clearly defined company strategy

Determine your company strategic priorities

Define your transformation ambition – ensure it aligns to your company strategy/strategic priorities

Get leaders involved

Build your transformation plan

Be clear on what success is

Gather resources and expertise

Choose the right enablers

Focus on culture and change management

Measure success

For more support on transformation please explore our range of thought leadership articles…

Resilience

Mark Easdown writes about resilience. Individual, Enterprise & Ecosystem Strategy & Planning & Ways of working. Let’s explore some scenarios across individual resilience, ethical resilience & the resilience dividend. At the individual level, the global pandemic, economic downturns, recessions and increase in uncertainty and anxiety highlight the need for resilience. As Diane L Coutu “How Resilience Works”, (HBR May 2002) observes, resilient people have certain defining characteristics…

Article written by Mark Easdown

Individual, Enterprise & Ecosystem Strategy & Planning, Ways of Working

““The world breaks every one and afterward many are strong at the broken places.””

““Resilience is the capacity of any entity – an individual, a community, an organisation, or a natural system – to prepare for disruptions, to recover from shocks and stresses, and to adapt and grow from a disruptive experience.””

““Don’t seek for everything to happen as you wish it would, but rather wish that everything happens as it actually will-then your life will flow well.””

“Kintsugi”: Kin meaning golden & tsugi meaning joinery, so “to join with gold”. In Zen aesthetics a different perspective emerges with broken ceramic pieces repaired using gold leaf and with great care thus highlighting the damaged history rather than hiding it. The object is given a fresh start, proudly wearing the flaws of its accident. Origins attributed to shogun of Japan, Ashikaga Yoshimitsu (1358-1408)

According to the Oxford English & Australian Concise Oxford Dictionaries, resilience is a noun, with key attributes;

Capacity to recovery quickly from difficulties, toughness

Ability of a substance or object to spring back into shape, elasticity

Recoiling, resuming original shape after bending, stretching, compression, shock, depression

Yet, the quotations above highlight a unique resilient frame of mind: “strong at the broken places” & “a fresh start, proudly wearing the flaws” & “don’t seek for everything to happen as you wish it would”. Judith Rodin believes “Resilience isn’t an inherited characteristic, it really is a skill” which would then enable you “to prepare for disruptions”.

Let’s explore some scenarios across individual resilience, ethical resilience & the resilience dividend.

At the individual level, the global pandemic, economic downturns, recessions and increase in uncertainty and anxiety highlight the need for resilience. As Diane L Coutu “How Resilience Works”, (HBR May 2002) observes, resilient people have certain defining characteristics;

They take a sober and down to earth look at the reality of the current situation

They search for and construct meaning for themselves and others, they build bridges to a better and fuller future

They continually improvise, they imagine new possibilities & put resources to new uses

Are resilient companies filled of optimistic people? Jim Collins in researching “Good to Great” sought counsel of Admiral Jim Stockdale to learn more…

“You must never confuse faith that you prevail in the end – which you can never afford to lose – with the discipline to confront the most brutal facts of your current reality, whatever they might be”

Admiral Stockdale was a pilot whos’ plane was shot down over Vietnam in 1965, he endured 7 ½ years of captivity and torture and a POW. He organised a system of discipline & communications with fellow POWs, refusing even under torture to offer his captors any intelligence. He earned the Congressional Medal of Honour. He observed the POWs who broke fastest where the ones who deluded themselves about the reality and severity of their ordeal, they were optimistic they would be out by next week, next month, Christmas ..

The Stockdale Paradox, is that in the face of hardship you must;

Maintain clarity about your reality ….. however at the same time … Find positivity and hope for the future

In turning around demoralised workforce or lagging business performance, executives and teams must maintain a sober analysis of current state and conjure up a sense of possibilities and brighter future states.

Constructing meaning out of circumstance, continually improving and staying future focus